As the federal budget’s housing policy changes start to sink in, the impact on the broader economy is starting to be realised.

One of the best bits of property analysis I’ve read in a while comes from Nerida Conisbee, Chief Economist at Ray White.

The federal budget’s housing measures are designed to push investor demand out of established homes and into new supply. It’s a reasonable goal. But as Nerida points out, there’s an unintended consequence that almost none of the commentary has picked up on, and I think it’s the most important part of the whole story: the changes are likely to reduce the number of homes that actually change hands.

That might sound like a dry, technical point. It isn’t. The number of property transactions is one of the great hidden engines of the economy and of state government revenue … and when it slows, the pain spreads a long way beyond the housing market.

Why transaction volumes matter more than prices

We’re all conditioned to watch house prices. But as Nerida’s analysis spells out, prices and the number of sales are two very different things. Also, over the past 25 years, sales volumes have been far more volatile than prices, swinging from fewer than 380,000 homes a year to more than 580,000.

The sharpest falls have always come when people’s ability or willingness to move is disrupted – tighter credit, higher rates, weaker confidence, or policy change. Volumes slumped through the late 2010s as lending standards tightened, then fell again as rates rose. By contrast, when rates fell and credit loosened through the pandemic, volumes roared back almost overnight.

The budget now adds a fresh disruption, and uncertainty alone is often enough to make people sit on their hands:

- Buyers may pause while they work out whether the changes affect prices, rents and future demand.

- Sellers may delay if they’re unsure how deep the future buyer pool will be.

- Existing investors have a clear reason to hold rather than sell (selling means giving up grandfathered tax treatment).

- New-build investors may hold longer too, knowing the future investor buyer pool for their property has narrowed.

And here’s why that matters so much.

A home sale is never just a change of ownership. It kicks off a whole chain of activity: buyers borrow, insure, move, renovate and furnish. Sellers repair, upgrade and often buy again. Every transaction supports a network of mortgage brokers, conveyancers, valuers, building inspectors, removalists, tradies and retailers. Rising prices can make people feel wealthier on paper … but it’s transaction spending that drives the economy.

The stamp duty time bomb for state budgets

Nowhere is this decline in transaction spending clearer than in state government coffers.

Stamp duty isn’t collected because homes exist, or because values rise on paper. It’s collected only when a property changes hands. That makes state budgets extraordinarily exposed to the level of activity in the market – not the price.

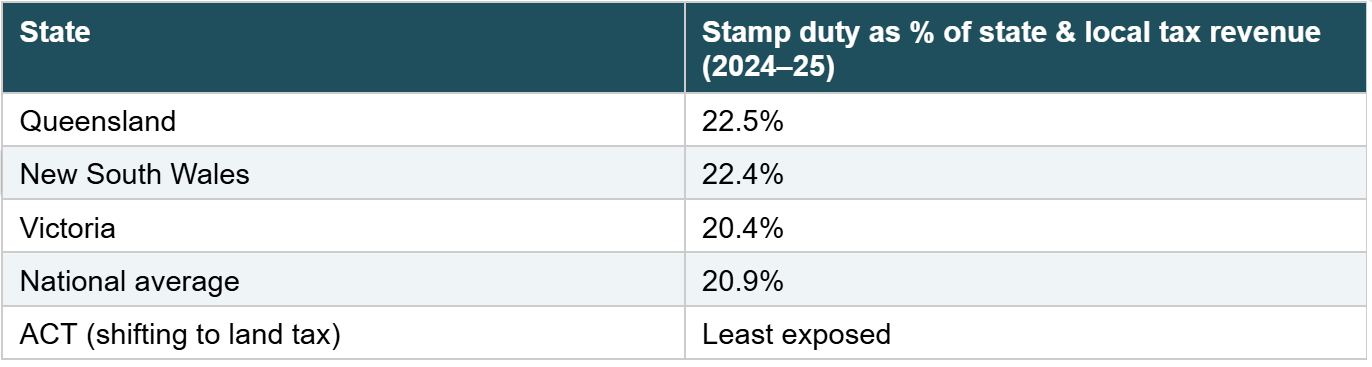

And the exposure is enormous. As the Ray White team highlights, in 2024-25 stamp duties on conveyances made up 20.9 per cent of all state and local government taxation revenue nationally. In some states it’s even higher.

So a fall in housing activity isn’t just a problem for buyers, sellers and property-related businesses. It’s a budget problem.

State governments lean heavily on revenue from people moving, upgrading, downsizing and investing … and stamp duty revenue has tracked the total value of residential transactions closely over the past decade. That value depends on two things: how many homes sell, and what they sell for. A high-price market with fewer sales can still leave a hole, because there are simply fewer taxable events.

Then there’s the supply of new homes issue …

Construction: where the homes are actually being built

Of course, the other half of the budget’s plan is to get more new homes built. So where is that actually happening?

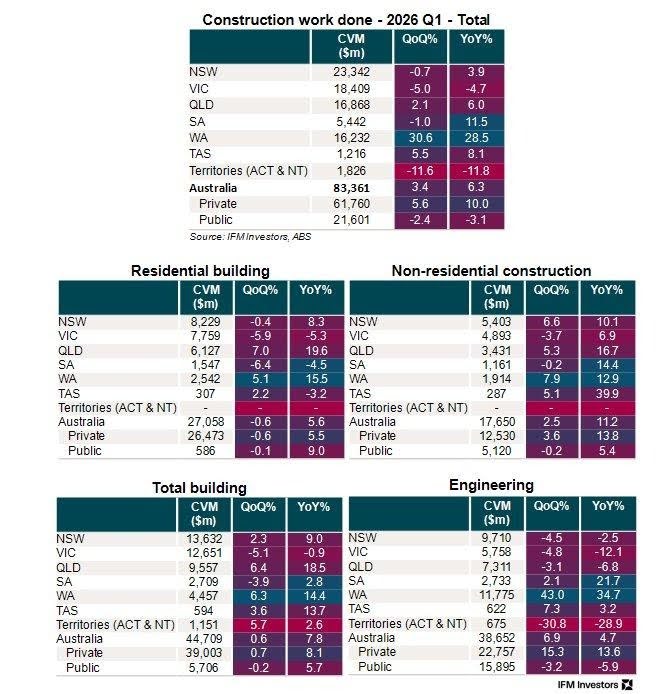

The latest construction figures below show the activity is heavily concentrated in a few states, and Western Australia is in a league of its own.

Nationally, total construction work rose 3.4 per cent for the quarter and 6.3 per cent over the year. But the standout is Western Australia, where this work surged 30.6 per cent in the quarter – up from 28.5 per cent on a year ago. We are seeing a genuine boom in WA.

In Queensland, construction is also up 6.0 per cent annually. In South Australia, it’s strong at +11.5 per cent, New South Wales is steady and Victoria is actually going backwards (−4.7 per cent over the year).

Residential building specifically is up 5.6 per cent nationally over the year, with Queensland (+19.6 per cent) and WA (+15.5 per cent) building away.

The encouraging news is that the supply pipeline is growing. The worry is that it’s growing in the states that already have land and labour to spare, not necessarily where the population pressure is most acute.

Less spending, less profit

It looks like the budget’s housing changes have been framed around increasing supply and affordability. But if they make investors and households less willing to transact, the damage won’t stop at house prices. It will flow through household spending, business activity and state government revenue.

We already have a housing shortage. A market where fewer homes come up for sale makes that shortage harder to fix. It also leaves state budgets more exposed to every wobble in housing activity.