Your retirement nest egg is doing well. Very well …

Good news for those keeping an eye on their super.

Research house Rainmaker Information estimates the typical MySuper default option returned 9.3 per cent in FY26 after fees and taxes – a fourth consecutive year of gains, and above the index’s 10-year average of 7.9 per cent, on top of last year’s 10.6 per cent.

MySuper is where your money sits if you never chose an investment option.

And it’s a perfect case study on why it’s best not to panic when the market wobbles.

Stay calm and invested

When conflict broke out in Iran, the index dropped 3.4 per cent in March .. scary stuff on a statement. Then it bounced 2.7 per cent in April and 2.3 per cent in May – a full recovery.

Rainmaker crunched the cost of panicking:

A member with $100,000 who switched to cash at the start of April ended the year more than $5,000 worse off than someone who stayed the course.

Under the bonnet, hedged international shares surged 15.4 per cent on the AI boom, while growth options returned 10.8 per cent, balanced 8.7 per cent, and capital stable 5.8 per cent.

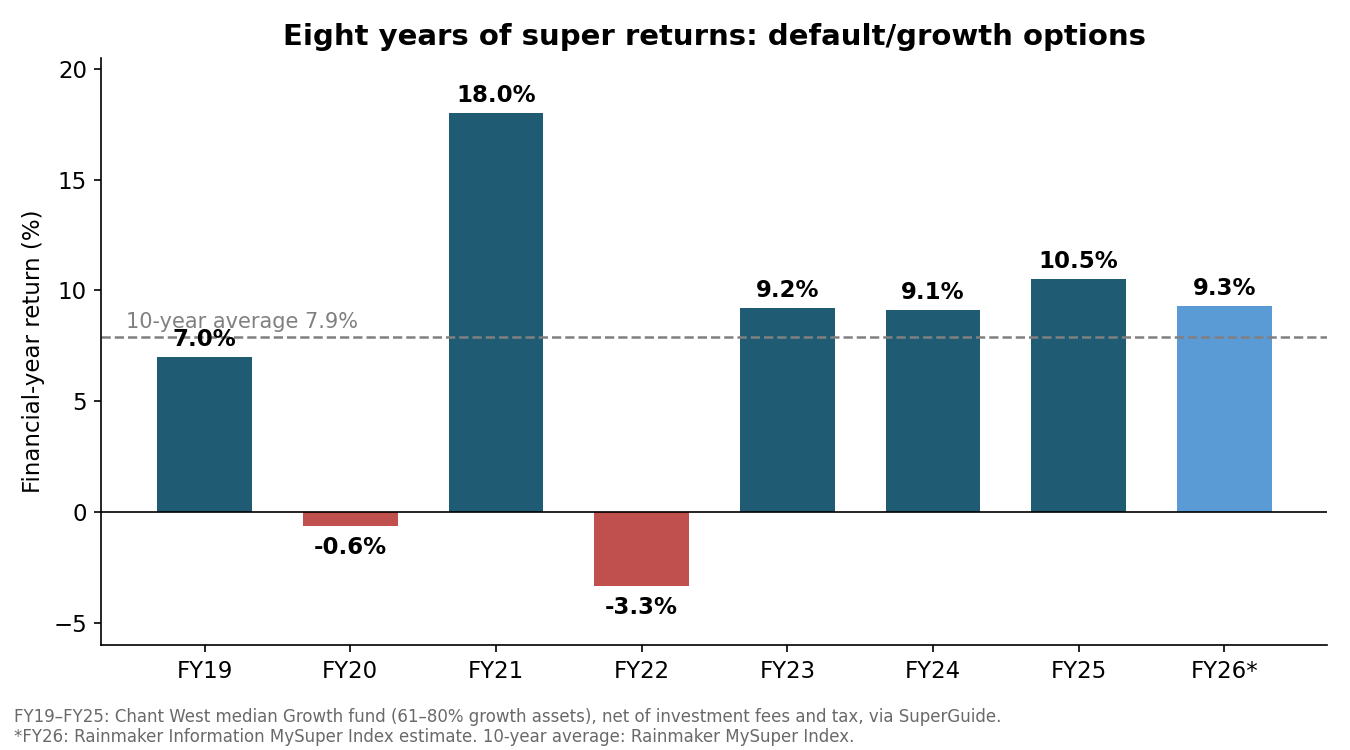

The below chart shows the past eight years in one picture, using Chant West’s median growth fund figures (the option most Australians are in) with Rainmaker’s FY26 estimate on the end.

Two down years – the COVID dip and 2021-22 – and six up, including the last four straight:

More super good news

Speaking of super quietly working for you:

Payday super is here – and it’s the sleeper reform that will fatten your nest egg even more.

As of 1 July, employers must pay super at the same time as wages – landing in your fund within seven business days of payday, not up to three months later under the old quarterly rules.

It sounds like plumbing, but the payoff is real: contributions start earning returns months earlier, every pay cycle, for your whole working life … and compounding does the rest.

Treasury’s modelling found a 25-year-old on the median wage ends up around $6,000 (roughly 1.5 per cent) better off at retirement from this timing change alone.

It also makes unpaid super harder to hide. An employer can’t quietly sit on your money for months …

Retirement on track

Super is Australia’s quiet-achiever success story.

Add in the new “payday super” rules, and the system gets an extra boost through better compounding and fewer delays.

Superannuation isn’t flashy. It’s long-term investing, not short-term gains (and losses), but leave it to ride the market waves and it delivers.

Sometimes four years in a row.