Government debt is under control … but we should be more worried about household debt.

I know there is a lot of commentary and panic around the size of government debt, and the fact that gross debt will pass $1 trillion in the next financial year.

Yes, it’s a big figure but Australia is a big economy.

Think of the economy as your house. The debt/mortgage is 37 per cent of the value of the economy/house. That is manageable.

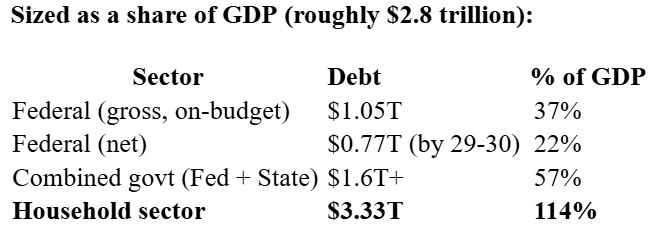

Despite all the hysteria around government debt, here are the facts. We have low government debt and extreme household debt:

Home is where the debt is

Household debt is approximately three times the size of Commonwealth gross debt, and roughly twice the size of total combined government debt in Australia.

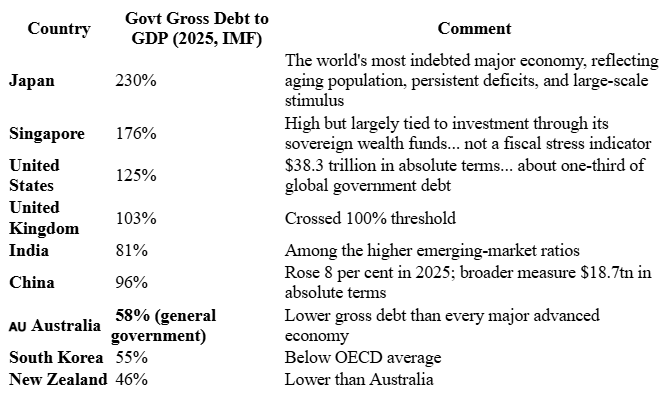

Now let’s compare Australia’s debt with our top eight two-way trading partners: China, Japan, United States, South Korea, India, Singapore, New Zealand, and the United Kingdom.

The International Monetary Fund measures general government gross debt (which captures all levels of government) and puts Australia at around 58 per cent for 2025:

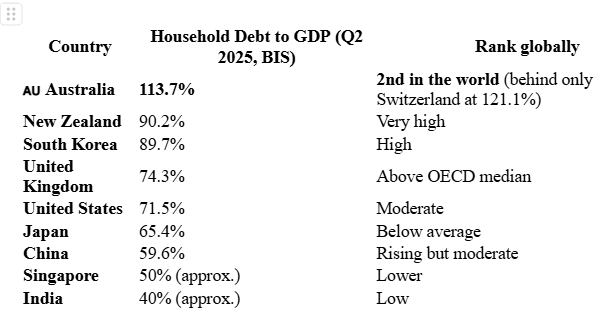

Household debt comparison

When it comes to household debt, the picture flips entirely.

The Bank for International Settlements (BIS) Q2 2025 data shows Australian households as among the most indebted in the world.

Australian households carry more debt relative to GDP than all eight major trading partners. It is roughly 1.6 times that of the US, 1.7 times Japan’s, and 2.9 times China’s as a share of GDP. The only major Western countries above Australia globally are Switzerland, Canada, and the Netherlands.

Hopefully that clears up the debt situation.

Balancing the figures

Now, let’s look at the economic and government policy implications of low government debt but extreme household:

- Monetary policy (interest rate) movements are unusually powerful. With household debt at 114 per cent of GDP and a high share of variable-rate mortgages, every RBA rate rise hits domestic demand harder than in the US, UK or Japan, where households are less geared and often hold long-term fixed-rate mortgages. The budget’s assumption of rising rates through the inflation peak, implies consumer demand will be hit harder than other economies.

- Fiscal space is real but politically expensive to use. Australia genuinely has fiscal headroom that Japan, the US and the UK do not. But the reason government debt is low is that the private sector (chiefly households via mortgages) has done the borrowing instead. Stimulus into a household balance sheet already carrying debt of around 114 per cent of GDP doesn’t translate into increased household spending, because marginal income is often directed toward debt repayments rather than consumption.

- Tax reform is a lever. The housing tax reforms in this week’s budget make more sense in this context. Replacing the CGT discount with indexation and limiting negative gearing aren’t just revenue measures – they’re structural tools aimed at slowing the growth of household debt, which is now the dominant financial risk to the economy. The Reserve Bank can’t address this through interest rates alone; only tax and supply-side policy can.

- Sovereign rating logic. Despite household debt at 114 per cent of GDP, Australia retains a AAA sovereign rating from all three major agencies. This is because sovereign ratings assess the government’s ability to pay, and a low public debt burden alongside a wealthy private sector (even if highly leveraged) is considered highly serviceable. Rating agencies’ greater concern is typically state-level finances rather than the Commonwealth.