After last week’s Reserve Bank interest rate increase, I warned of the possibility that rising rates coupled with rising petrol prices had the possibility of crushing Australian household budgets.

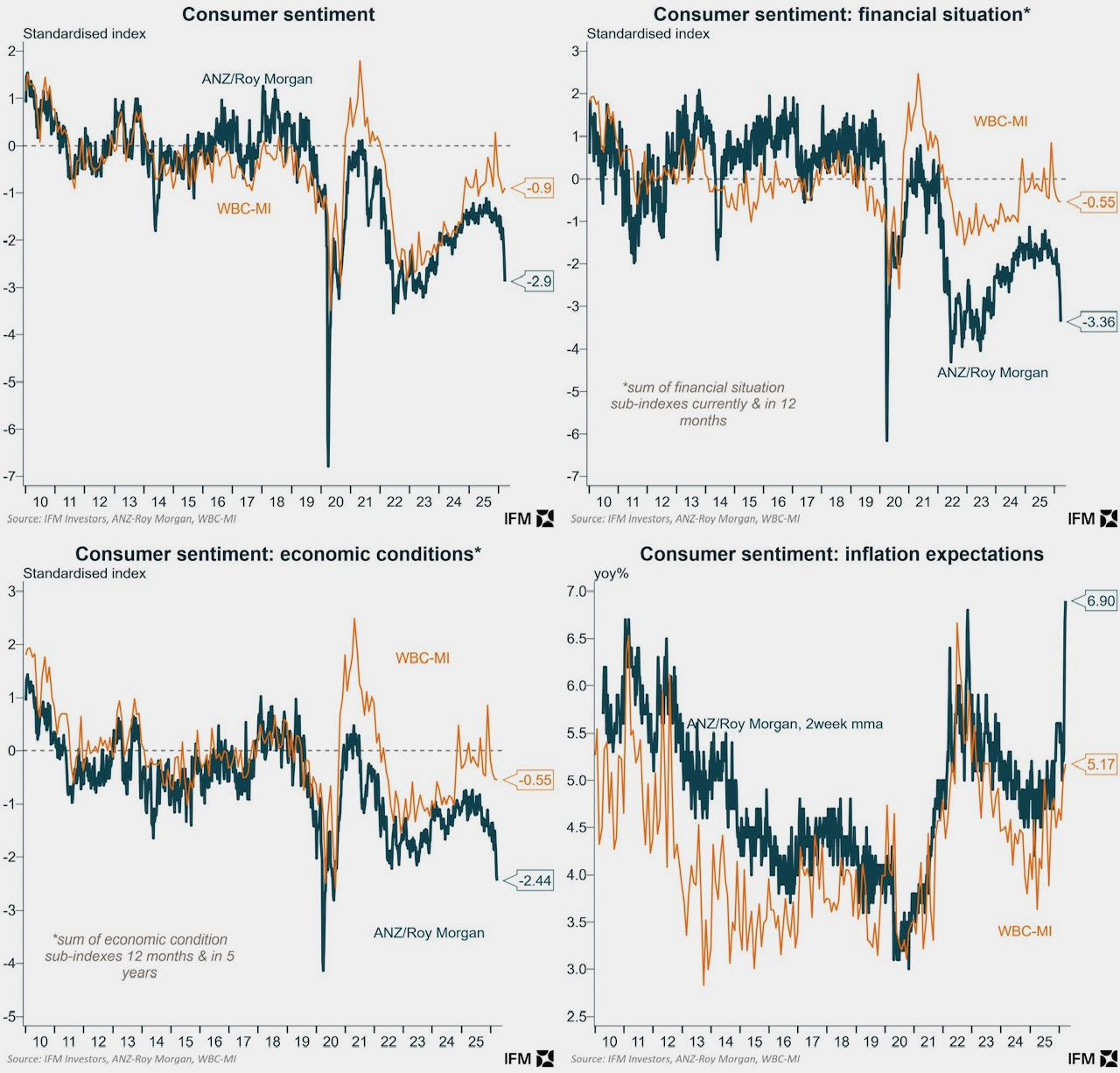

Reinforcing my point, this week’s ANZ-Roy Morgan consumer confidence figures are down 20 per cent – the worst result since the oil crisis in 1973.

Consumers expect inflation to soar to 6.9 per cent, while the number of people who believe it is a good time to buy a large household item is in freefall.

The RBA’s 0.25 percentage rate rise this week, taking the cash rate to 4.1 per cent, has added about $94 a month to repayments on a $600,000 home loan. It was the second consecutive increase, following the February board meeting hike, and a third straight rise is expected at the next RBA board meeting in May.

Add the two consecutive rate rises together and average the repayments on the average home loan ($694,000-$736,000) will be up around $200 a month … After a third hike, it would be almost $300 a month.

Then add the extra $100 a month ($25 a week on a 60 litre tank) to fill a car since the Middle East crisis started lifting global oil prices, and Australian household budgets are being hit hard. The lift in petrol prices is about the same as a 0.25 per cent rise in interest rates.

The economic mirror

These numbers matter because household spending drives the economy. Confidence feeds itself: the worse people feel about their finances, the less they spend – and the slower the economy goes.

Right now, ordinary Australians are feeling the squeeze from all sides – higher interest rates, rising petrol prices, and inflation – all with global supply chain uncertainty in the mix.

Everyday life is costing more. There’s less for groceries, expenses and even little treats that make life enjoyable. This isn’t coming tomorrow – it’s happening now. Planning ahead, keeping a close eye on your budget, and preparing for tighter months isn’t doom and gloom. It’s smart money management.

Watch the numbers. Watch your own spending. Watch the bigger economic picture. When households tighten up, the economy often follows.

Practical steps to protect yourself:

- Track your spending: Know where every dollar goes and identify areas to cut back.

- Prioritise essentials: Focus on groceries, clearing debt, bills, and school costs first.

- Build small cushions: Even modest savings can reduce stress in lean months.

- Plan for bills ahead: Account for rising interest rates and fuel costs in your monthly budget.

- Stay informed: Keep an eye on economic indicators so surprises don’t catch you off guard.

Stay alert. Be careful. Plan wisely.