Your property will be worth more now, so it’s time to act.

Homeowners need to start taking advantage of the increase in their property’s value by negotiating a better home loan interest rate with their lender.

The general rule of thumb is that the more equity you have in your property, the better the interest rate you’ll get from a lender. Financiers believe the higher the equity you have in your property, the lower the risk you will default on the loan, so the better the interest you receive.

Over the last few years many people who took out a loan based on a small level equity in the property would now have a much larger stake, given Australia’s property boom. And that could mean a better interest rate.

Do the maths

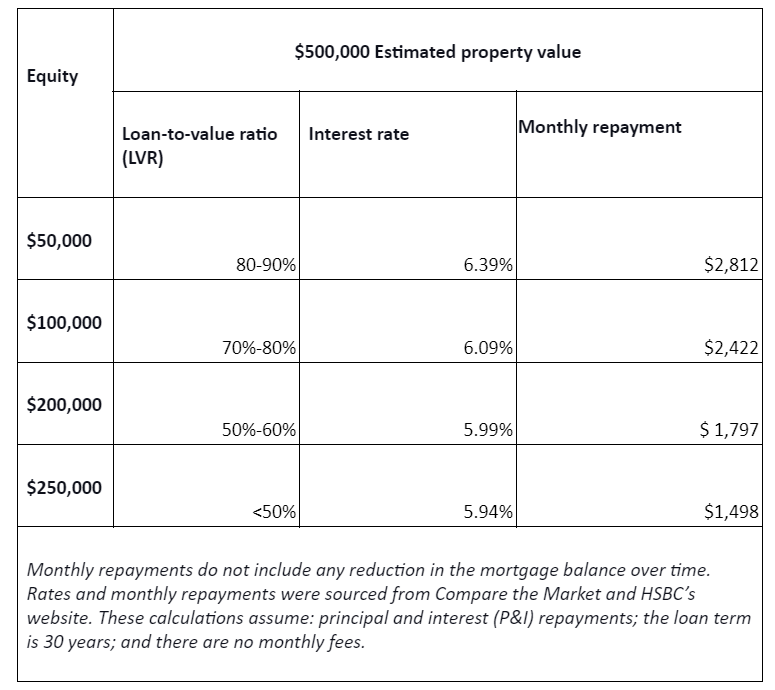

Lenders base your home loan rate on your ‘Loan to Valuation Ratio’, that is the size of the loan against the value of the property. An analysis by Compare the Market found that rates for borrowers with a LVR of 50-60 per cent could be up to 0.40 per cent less than some of the top rates on offer for borrowers with an LVR of 80-90 per cent.

For a property valued at $500,000, that could be a difference of $1,015 on a borrower’s monthly repayments. That is a massive saving.

The national median house value was 32 per cent higher in May 2024 compared to May 2019, according to figures from CoreLogic, meaning a large number of Australian property owners could be sitting on untapped equity.

Property owners who have not refinanced during the past few years could be missing out and need to act now.

If you have been paying off your mortgage for quite some time, it’s also likely that the value of your property has increased. People with a lower LVR are often entitled to lower interest rates because their loans are seen as less risky. This is their trump card.

Since the rates tightening cycle began in May 2022, a borrower with an average loan size of $626,000 is potentially paying $1,619 more each month.

Just because your LVR has decreased, doesn’t necessarily mean the bank will automatically drop your rate. You’ll likely have to do the heavy lifting to get that discount.

If you’ve recently undergone renovations or believe your property value has increased, you may have to ask the bank for an evaluation so they can determine whether you will qualify for a lower rate.

But even if your LVR hasn’t improved, you’ve got to make sure you’re on a competitive rate and not paying more than you need to be.

It doesn’t always pay to be loyal when there’s a 0.45 per cent difference in home loan rates, which can add up to be tens of thousands of dollars more over the life of the loan.