The CommBank is experiencing a surge in home loan pre-approvals – up 12 per cent since the last two interest rate cuts. The average borrowing amount has also increased 13 per cent, compared with this time last year.

Ray White chief economist, Nerida Conisbee, has done a deep dive into how this will shape the property market, but also, how rate cut cycles can have differing impacts on values.

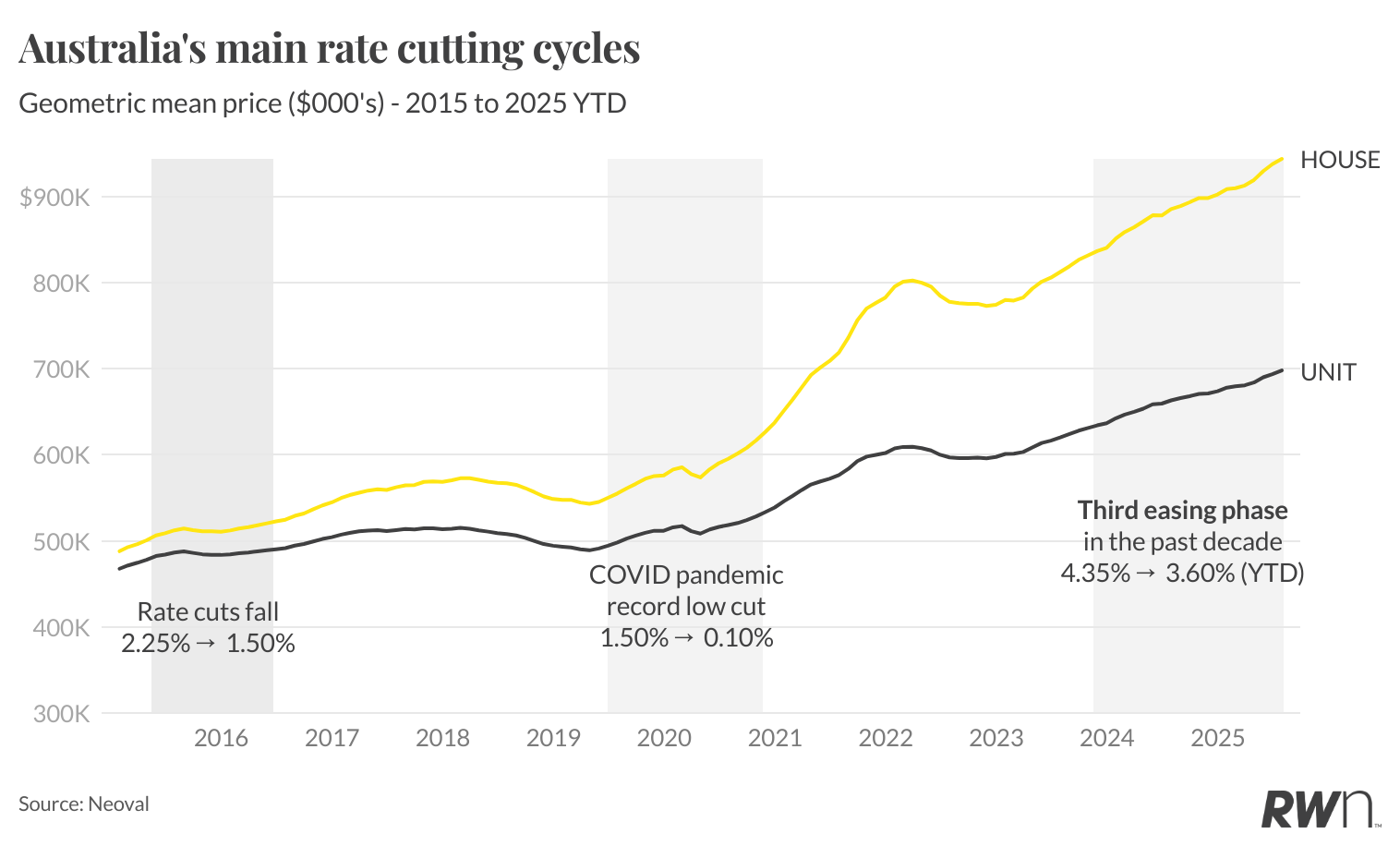

Australia has had three major interest rate cutting cycles since 2015, each delivering vastly different impacts across the housing market.

The Reserve Bank’s gradual easing from May 2015 to May 2016 saw rates fall from 2.25 per cent to 1.50 per cent, followed by a more aggressive round of cuts from June 2019 through the COVID-19 emergency period, which brought rates down to a historic low of 0.10 per cent by late 2020.

The current easing cycle, which began in 2024 from multi-year highs above 4 per cent, marks the third distinct phase of rate cuts within a decade. Suburb-level analysis by Ray White shows that each cycle has benefited entirely different segments of the property market, with the most responsive areas shifting significantly depending on the economic context and buyer demographics of each period.

2015-2016 cycle: The shift to affordable regional coastal markets begins

The first cutting cycle from May 2015 to May 2016 saw the Reserve Bank reduce rates by 0.75 per cent in response to moderating economic growth and subdued inflation.

This gradual easing primarily benefited coastal lifestyle markets within commuting distance of major cities, with NSW’s Central Coast emerging as the standout performer.

These suburbs, typically priced between $800,000 and $1.2 million at the time, attracted people looking for coastal lifestyles within commuting distance to Sydney. While COVID led to a shift to regional areas, the reality is that it had already started quite some time earlier.

2019-2021 cycle: Premium Sydney suburbs dominate the rate cut response

The most aggressive cutting cycle began in June 2019, then accelerated dramatically during the COVID emergency period as rates plunged from 1.50 per cent to 0.10 per cent.

These unprecedented rate cuts led to the strongest responses in Sydney’s premium suburbs. These were predominantly million-dollar-plus markets, reflecting how the combination of ultra-low rates and fiscal stimulus created a pronounced “wealth effect” favouring established property owners looking to upgrade or invest in premium locations.

2024-2025 cycle: Affordable outer suburbs emerge as the new rate cut champions

The current cutting cycle, beginning from the highest rates in over a decade, has fundamentally reversed previous patterns by most benefiting affordable, outer suburban areas.

Perth has dominated this cycle, with areas like Midland-Guildford (15.6 per cent growth), Mandurah (15.5 per cent), and Balga-Mirrabooka (15.4 per cent) leading national growth rates. Adelaide’s outer suburbs have also responded strongly, with Smithfield-Elizabeth North posting 14.4 per cent growth. These areas, typically priced between $550,000 and $750,000, represent traditional first home buyer territories where borrowing capacity improvements from rate cuts have the greatest impact.

It’s a dramatic shift from previous cycles, with the most rate-sensitive areas now concentrated among affordable markets, rather than lifestyle or premium segments. It reflects how Australia’s housing affordability crisis has fundamentally changed who benefits the most from monetary easing.