With the thresholds for the Medicare Levy Surcharge about to change, it’s worthwhile making sure you’re not caught, particularly if you’ve had a pay rise this year.

In a nutshell, the Medicare Levy Surcharge (MLS) is an additional tax for high-income earners who don’t hold an appropriate level of private hospital cover. If you earn more than $97,000 as a single or $194,000 as a couple/family this financial year and don’t hold an eligible private hospital insurance policy throughout the entire financial year, you’ll incur a surcharge.

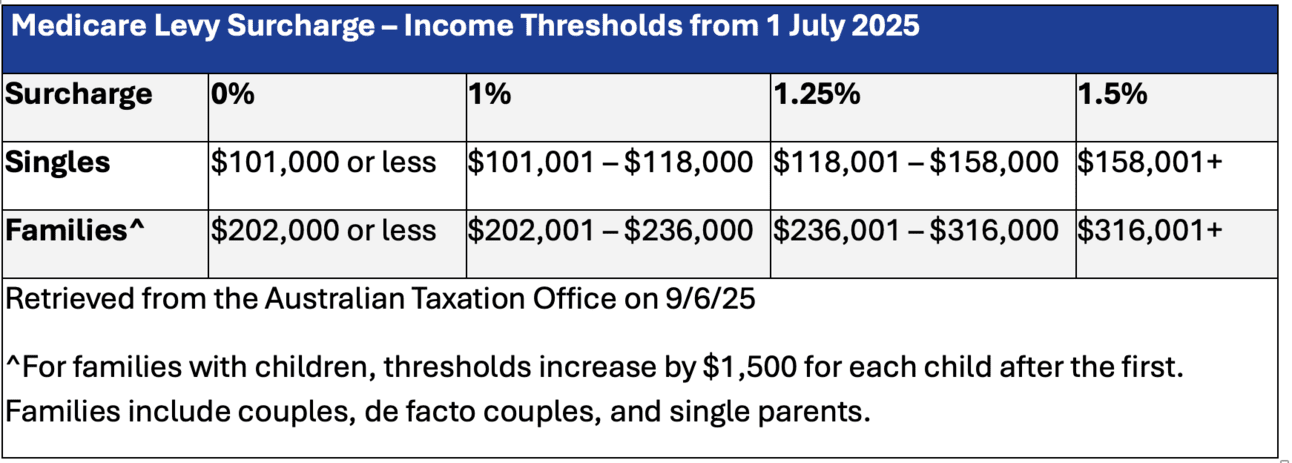

But from 1 July, the thresholds are changing. Singles who earn more than $101,000 or couples/families earning over $202,000 who don’t hold a hospital policy or a combined hospital and extras health insurance policy will incur a surcharge for every day in the 2025-26 financial year they don’t have cover.

The surcharge varies based on your income and climbs the higher your taxable income is.

You may have been one of the lucky Aussies to receive a pay increase above $97,000 this financial year, but unless you hold hospital cover, you’re likely to be stung this tax time. And the kicker is that the MLS is applied for every single day during the financial year that you haven’t held private hospital cover if you’re earning over the minimum threshold. You can’t just wait until 30 June to take out a policy to avoid paying the tax.

The good news is that if you think you’ll get a new job in the 2025-26 financial year or you’re in line for a pay increase that pushes you over $101,000, you have time to lock in hospital cover ahead of 1 July and avoid paying the MLS by maintaining an eligible policy for the full financial year. If I had the choice between getting stung with an extra tax or having hospital cover that could help if I needed it, I know what I’d choose.

Picking health cover

There are so many policies available, and it can be confusing to know what’s what, but you need hospital cover or a combined hospital and extras policy to avoid paying the MLS. Extras can still be great for those medical treatments you receive out of hospital, like general dental, optical, physio and psychology, but it doesn’t have an impact on whether you pay the MLS or not.

Another thing to be wary of is basic hospital policies. While they help you avoid paying the MLS, many basic options have minimal cover or virtually none at all. If you’re looking for a policy that you’d be able to utilise, consider a Bronze policy at a minimum. A standard Bronze policy covers 18 unrestricted clinical categories relating to things like ear, nose and throat treatment, joint reconstructions and gynaecology.

For something more comprehensive, you’d want to consider a Silver, Silver Plus or Gold policy. Gold is the most comprehensive option available, covering all 38 unrestricted clinical categories.

The health insurance experts at Compare the Market reckon these are the top tips for locking in health insurance:

Sweeten the deal

There are some rewards, perks and incentives on offer, such as frequent flyer points, weeks free, and waived waiting periods on eligible extras services. See if you can get a great value policy and a little extra on the side to stretch your dollar further.

Compare apples with apples

There are so many options available and while some policies have similar names, the services they offer aren’t always the same. Be sure to check your policy brochure for inclusions, exclusions, waiting periods and more that will apply.

Don’t be stung with a loyalty tax

If you’ve been with the same health insurance provider for some time, you may not be getting the best value. Always compare other brands on the market to see if you can pay less for the cover you need.