This week brought two major economic forecasts and one uncomfortable message: Australia is stuck in the slow lane.

Growth is losing momentum, but inflation is still running too hot – two key ingredients for delaying rate cuts even longer.

The good news? There is a silver lining in the clouds.

Here’s what happened:

Australia’s bigger picture

I did some sobering reading this week. Two major reports – one from Deloitte and the other from the International Monetary Fund – that both paint a challenging picture for Australia’s economy.

Deloitte has slashed its 2026–27 growth forecast from 1.9 per cent to just 1.3 per cent, with the economy expected to grow only 1.1 per cent in the year to December 2026.

All up, Deloitte tips 2.2 per cent growth in 2025-26, 1.3 per cent in 2026-27 and 1.9 per cent in 2027-28 – meaning the economy limps along at under 2 per cent for two years, the longest stretch of sub-2 per cent growth since the early-1990s recession …

The culprits are familiar: rising interest rates, weak consumer and business confidence, stalling housing investment and a drawn-out cost-of-living squeeze. Deloitte notes business investment is subdued outside one bright spot … data centre construction.

The International Monetary Fund came to a similar conclusion, trimming Australia’s 2026 growth forecast to 1.9 per cent from 2 per cent, which ranks us 18th of the 30 large economies it models.

The Government’s counter is fair enough. It points out that Australia is still expected to outpace every major G7 economy except the United States in both this year and next.

But the sting is in why growth is being marked down: inflation won’t behave.

As the RBA’s Chief Economist Sarah Hunter put it this week, “We may need some period of low inflation and higher unemployment to bring expectations back down if they start drifting up.”

Which brings me to …

The inflation table nobody wants to top

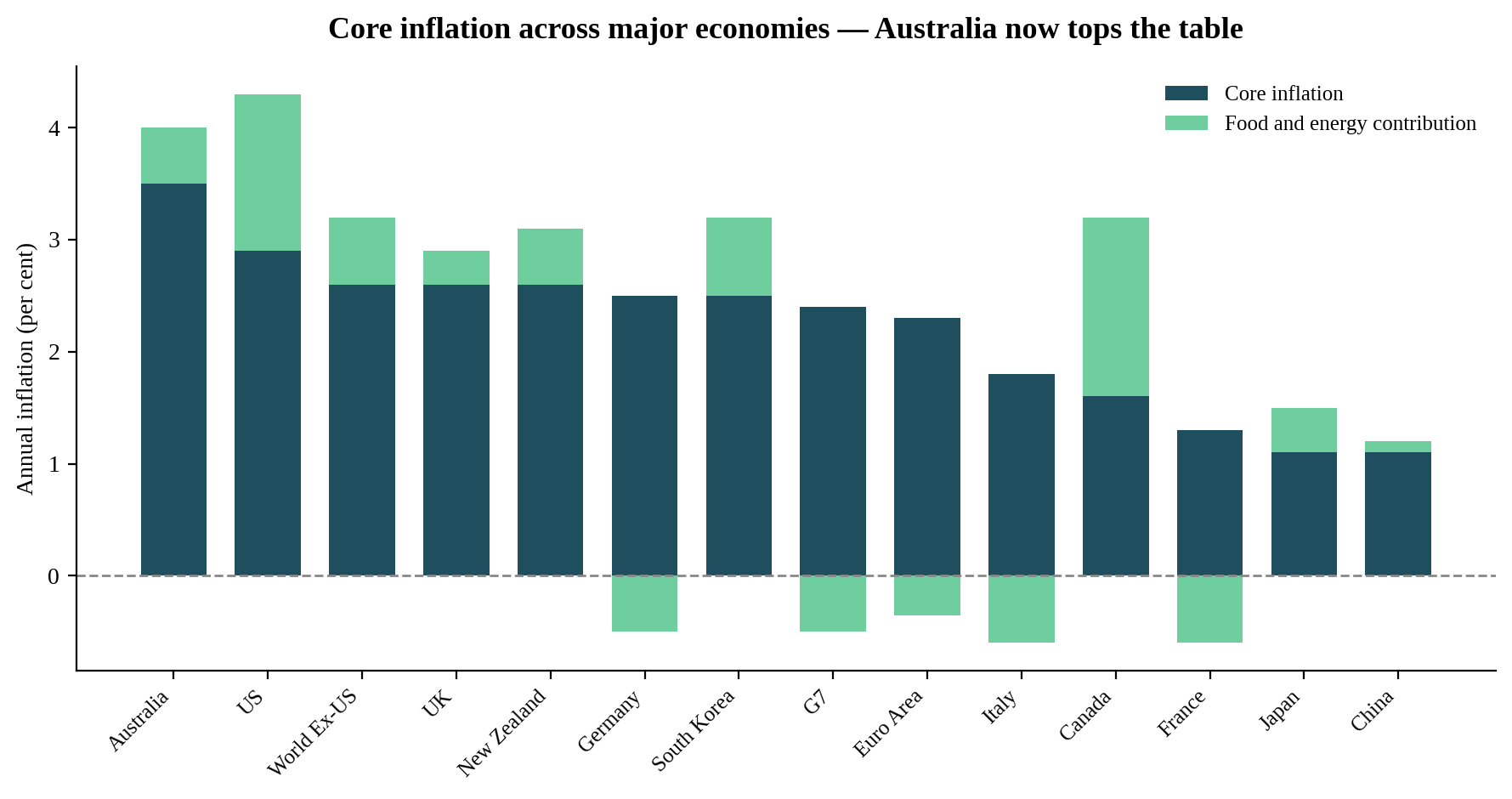

Australia is leading the world – in inflation.

This chart by IFM investors shows where we sit compared with other developed nations. On the measure economists call “core” inflation – which strips out food and energy – Australia is running at about 3.5 per cent, the highest among the major economies.

We’re above the US, the UK, New Zealand, the G7 average and the euro area. Add food and energy back in, and our headline inflation rate is around 4 per cent. That’s consistent with the IMF’s forecast that Australian consumer prices will rise by 4 per cent in 2026 – more than most advanced economies.

So when your inflation is the highest in the developed world, the central bank doesn’t cut rates.

That’s the simple, uncomfortable arithmetic behind all the “no cuts until 2027” talk … and why some economists are even flagging the risk of another hike.

But, and here’s the silver lining, the next chart hints the medicine may finally be working.

Hope for a future rate cut

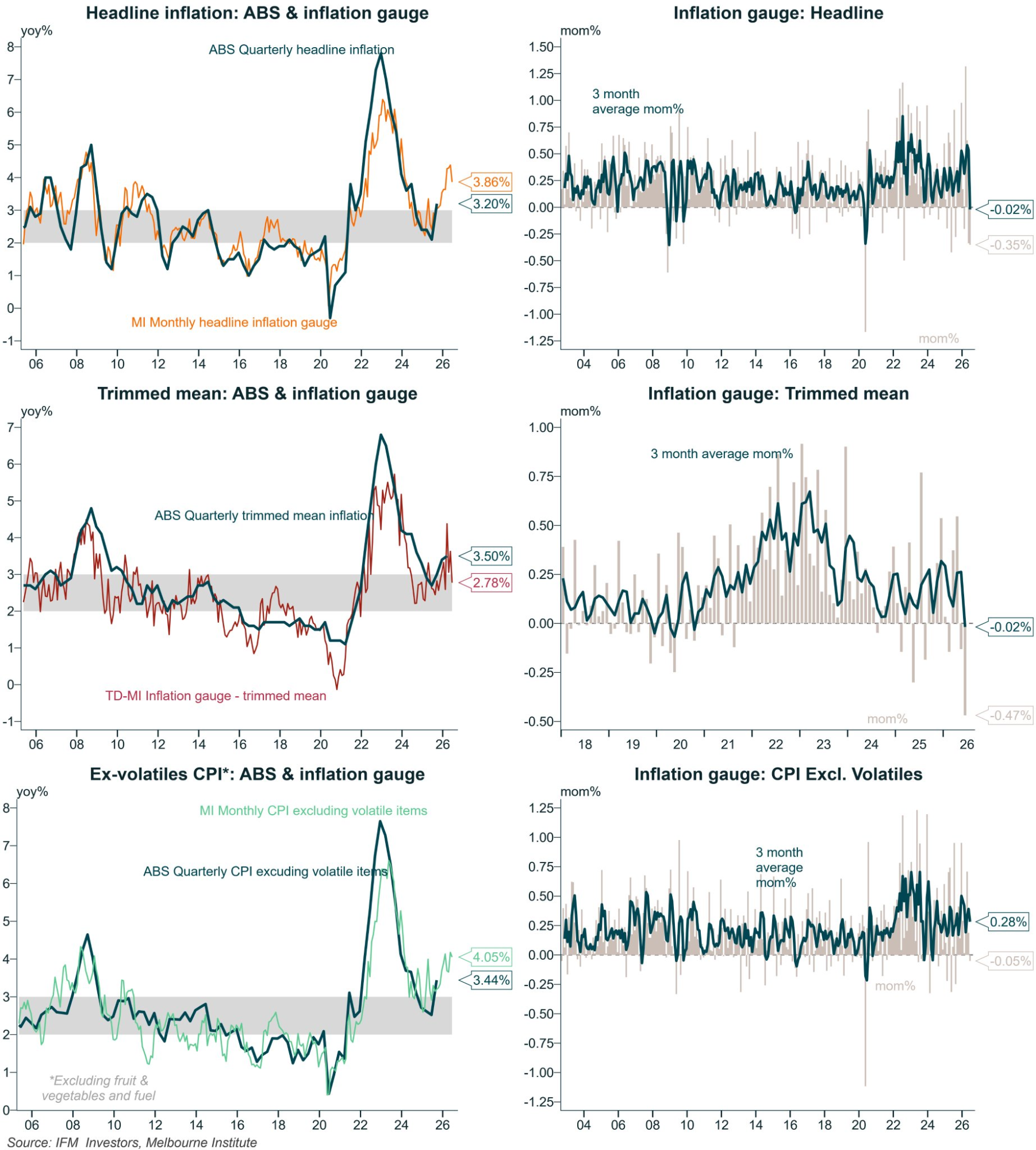

IFM Investors’ charts of the Melbourne Institute’s monthly inflation gauge show the annual numbers are still ugly: the headline measure is running at 3.86 per cent, above the ABS quarterly reading of 3.20 per cent, while the measure excluding volatile items such as fuel, fruit and veg sits at 4.05 per cent.

Look closer, though, and the momentum is turning.

The gauge’s ‘trimmed mean’ (and the RBA’s preferred way of measuring underlying inflation) has eased to 2.78 per cent – back within the RBA’s 2 to 3 per cent target band.

And in the latest month, prices actually went backwards: the headline gauge fell 0.35 per cent and the trimmed mean fell 0.47 per cent, dragging the three-month averages to basically zero.

One month of falling prices doesn’t make a trend, and the RBA will want to see it confirmed in the official quarterly CPI before it softens its language.

But if the monthly gauge keeps cooling like this, the rate-cut conversation could restart earlier than the pessimists think.

That said, don’t bank on it and budget for rates staying put … but watch the next couple of monthly readings.

The economic forecasts can and do change.