Interest rates will stay high well into next year, making household debt management a huge priority for Australians.

Loan repayments are crippling family budgets at a time when cost of living pressures are squeezing spending and credit card balances rise to plug the gap.

Debt consolidation has become the ultimate cure to manage the total debt burden as Aussies work to crunch over $18 billion in credit card balances accruing interest.

Reserve Bank data shows the average lending rate for credit card balance is at whopping 17.98 per cent so debt consolidation – rolling multiple loans into one – has become a popular way to manage debt with a single due date, repayment amount and interest.

We know interest rates on credit cards and some personal loans can be upwards of 20 per cent and home loan rates are typically much cheaper at around 6 per cent.

Debt consolidation is where you consolidate all your high interest debt into one low interest loan. It’s a good strategy if it’s done well, but you need to think it through and be disciplined about it.

Any high-interest debts should be treated with caution – you may want to reconsider any debt where the costs in interest and fees far outweighs the benefit you get from the purchase.

Even if you think you can wing a better rate, or if your lender extends the loan term, you may pay more in the long run. For example, rolling a high interest credit card debt into a low interest home loan is sensible. Except if you turn that short term high-rate loan into a 30-year long term low interest loan. In the end, you’ll pay more in interest.

The key to debt consolidation is rolling that credit card balance or that outstanding Buy Now Pay Later into the home loan and then setting a strict time frame to pay that amount off the mortgage. Think about using the credit card interest you’ve saved on the switch to pay extra off the mortgage.

Then make sure you don’t use that as an excuse to start racking up further consumer debt. It may be a relief to see that outstanding credit balance wiped out but it’s still there … just in a different loan.

The worst thing you could do is to start racking up new debt using the available credit on the card. Start budgeting and reducing expenses to avoid this happening.

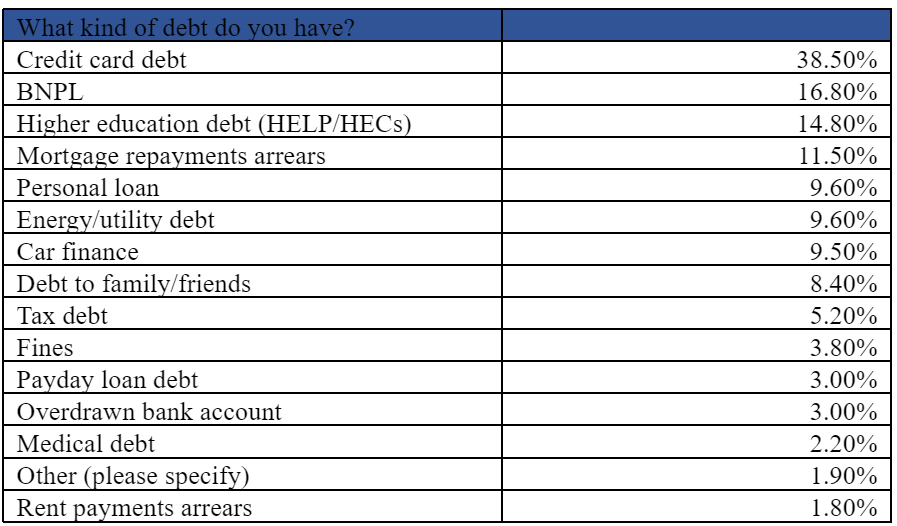

A Compare the Market survey showed almost two-thirds of Australian adults have some form of debt.

The nation’s most common types of debt include credit card debt (38.5 per cent), Buy Now Pay Later (16.8 per cent), higher education (14.8 per cent) and mortgage repayment being in arrears (11.5 per cent).

The data also showed more than 9 per cent of people surveyed have personal loans, car loans and energy or utility debt. Less than a third of Australians said they did not have any debt.

After 13 post-pandemic rate rises, people are taking on debt to afford everyday essentials like electricity, petrol and groceries. And that creates a vicious circle while interest rates stay at these high levels.

Top tips for considering debt consolidation

- Block out an hour in your calendar to shop around for a loan with a low interest rate, with conditions that work for you. Go to online comparison websites to see how your home loan stacks up and review any options to refinance to a better rate to use for the consolidation.

- Make sure the repayment terms and schedules align with your personal circumstances. For example, if you get paid on Tuesday, maybe schedule the loan repayments for Wednesday or Thursday, so you reduce any risk of paying late fees and further interest.

- If you are up to your eyeballs in debt, it could be time to speak to a professional or talk to your bank or lender about hardship programs, payment plans and payment extensions.

- Check your credit score. It’s important know but research shows that 40 per cent of homeowners have never checked their credit score. This is what lenders use to assess your risk profile when assessing your eligibility for a loan and the interest they’ll charge.

- A good credit score allows you to negotiate a better interest rate on a new loan and improves your chances of being approved.

Getting familiar with your credit score could help you set some goals to get your finances in better shape for refinancing. They are often free to download from your lender’s website or comparison sites.

If you need additional support, the National Debt Helpline is free to call on 1800 007 007.