The 0.25 per cent cut to interest rates could leave an extra $100 a month in the pockets of mortgage holders. And most lenders have already indicated they’ll pass on the full cut to borrowers.

It’s great news if you are under mortgage stress … but there is more you can do to ease it. Here’s how to negotiate with your lender.

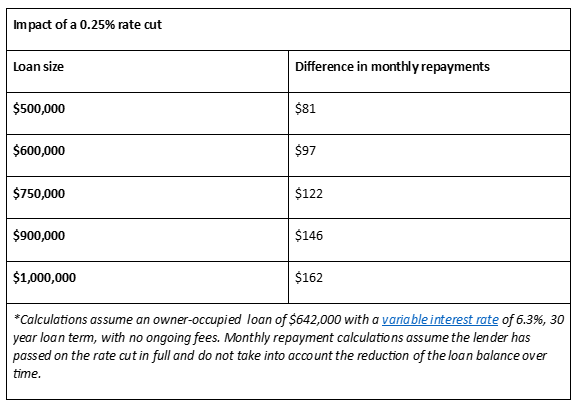

What a 0.25 per cent cut means

Monthly repayments on an average $642,000 loan with a variable interest rate of 6.3 per cent will be cut by as much as $104, or around $1,248 over the course of the year. The exact reduction would depend on the size of the loan, if the lender passes on the potential rate cut and the current interest rate.

But don’t forget you can negotiate an even bigger rate cut by checking whether you’re on a competitive home loan interest rate or not.

How to get an even better rate

A lot of people think they’re trapped with their lender, but this isn’t the case. There are options out there and you’ll notice that even if your bank doesn’t directly lower your rates, they’ll be offering cheaper deals out there to new customers. This tells me that banks can and should be offering lower rates to their existing customers, but sadly, they’ve been getting away with slugging a loyalty tax for too long. It’s price gouging at its finest.

There are three steps to take before attempting a negotiation with the banks:

Step 1 – Before you ask for a lower rate, arm yourself with information. You should know your lender’s lowest advertised rate.

Step 2 – Next shop around and see what other offers are available. You might find even cheaper rates or enticing incentives like cashbacks.

Step 3 – Finally, use a calculator to work out what you could be saving. Knowing the money you could be clawing back is great motivation. You should feel empowered to negotiate.

The worst thing that can happen is that your bank will tell you ‘no’ and then you’re free to move on to a different lender.

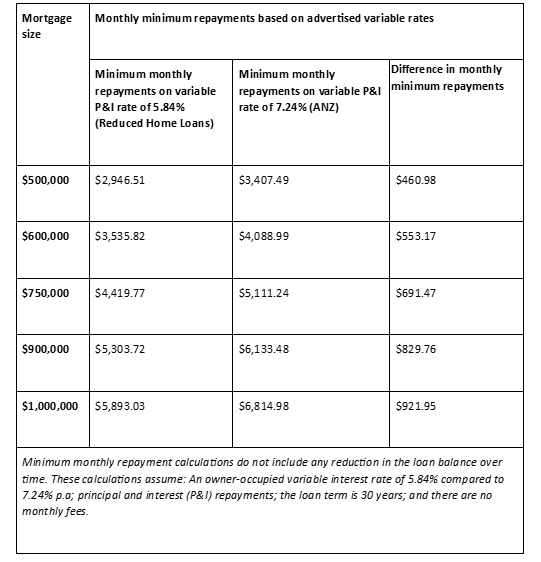

Compare the Market analysis conducted in February found a whopping 1.4 per cent difference between the highest (7.24 per cent) and lowest (5.84 per cent) advertised rates for some variable loans. That’s the equivalent of almost six 0.25 per cent RBA rate cuts.

Refinancing may save you thousands of dollars over the life of your loan but look out for the following when refinancing:

- Fees – Ask the new lender to waive upfront fees.

- Break costs – If you refinance from a fixed-rate loan before the fixed term is up, you could incur significant break costs.

- Cashback deals – The allure of cold hard cash can be tempting but also consider the interest rate being offered.

- Avoid an ugly revert rate – Fixed rate loans usually revert to a standard variable interest rate after a pre-determined amount of time, which is often much higher than the market average variable rate.