Yesterday Westpac hiked its fixed rate home loan for the second time in less than two weeks, and today the CBA followed suit. Which begs the question: Is it time for a fixed-rate home loan?

Three-year fixed-rate mortgages are tied to market rates of that term because banks borrow or hedge interest rate risk at those market-determined rates. The RBA’s decision earlier this week to abandon its yield curve target means banks have lifted fixed rates for new borrowers to maintain their margins.

Four lenders have hiked their fixed rates twice in the last month: CBA, Westpac, AMP and BDCU Alliance Bank. It’s likely this list will grow.

“With improving economic conditions and banks scrambling to announce interest hikes, it is wise to start preparing for this shift in the interest rate environment,” says Catherine Mapusua, Head of Lending at Australian digital lending and payment provider WLTH . “It is important to consider whether a fixed rate suits your needs, as this can restrict additional repayments and may charge break fees if there is a change in your circumstances.

“If you change banks, sell the property, or need to break the rate of your repayments, you risk charges that can be from a couple of hundred to several thousand.”

Latest figures from ABS lending indicators show 45.3 per cent of people are choosing to fix their home loans.

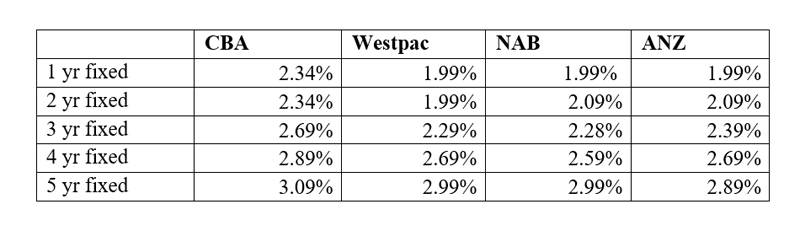

Lowest big four bank owner-occupier home loan rates

Source: RateCity.com.au. Note: CBA and Westpac rates are for a loan to value ratio of up to 70%.

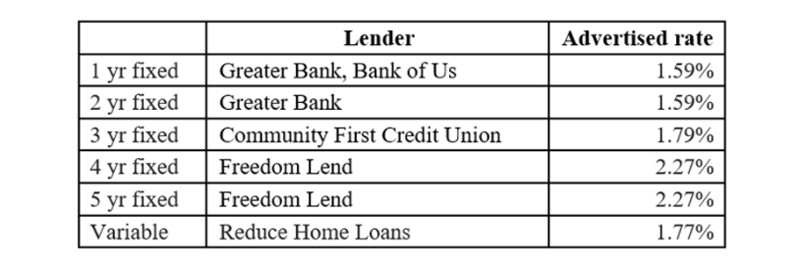

Lowest rates on the RateCity.com.au database

Source: RateCity.com.au. Note: Rates are for owner-occupiers paying principal and interest. Some LVR and location requirements apply.

To lock in your fixed rate or not?

If you decide to go with a fixed-rate home loan, you have another big decision to make: to lock or not?

“If you have a fixed-term interest rate, consider paying a lock fee,” says Mapusua. “This can help secure your fixed rate on offer at the time of settlement, protecting you from rate increases before the loan is advanced.”

A ‘rate-lock fee’ is a fee a customer pays to lock in the fixed rate on offer at the time of application (or any time before settlement), protecting them from any rate rises during the process. The ‘lock’ typically last for around 90 days, but this can differ between lenders, and the cost can run into thousands of dollars.

RateCity analysis shows on a $500,000 3-year fixed rate at 2.26 per cent loan with the average big four banks, if the rate rises to 2.46 per cent before the application is processed, borrowers will pay an extra $2,935 over this term if they don’t lock in their rate.

In this scenario, the borrower will be better off if they pay the typical rate-lock fee of up to $750, but only if the lender hikes rates in that time.

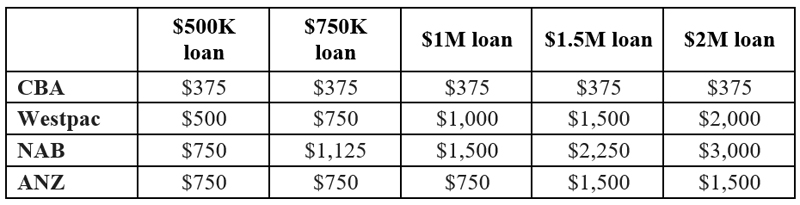

Big bank fixed rate lock fees

Source: RateCity.com.au.

CBA charges $750 per lock, regardless of loan size however the fee is currently discounted to $375.

Westpac charges 0.1 per cent of the loan balance.

NAB charges 0.15 per cent of the loan balance.

ANZ charges $750 per $1 million of lending.

Yes, paying the lock fee provides an ‘insurance policy’ against rate rises and gives the borrower the certainty of knowing what the repayments will be during the fixed period.

However, there is no guarantee rates will rise in the time before settlement, so a borrower can pay the fee unnecessarily. Plus, taking out a rate lock too soon could see it could expire before settlement.