Did you know you could get a lower interest rate and improve the value of your home while making it more energy efficient as well?

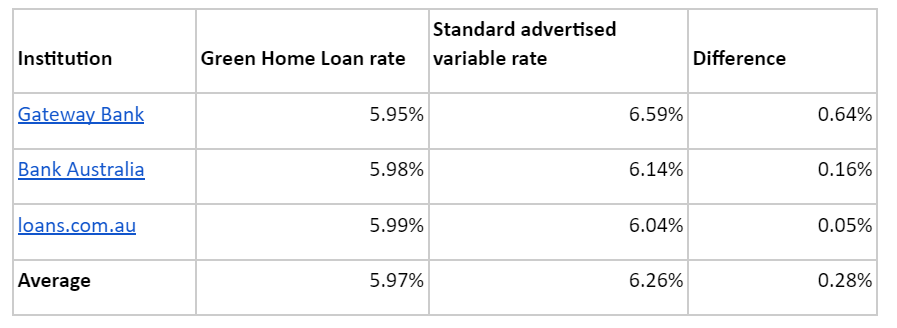

According to a Compare the Market analysis, borrowers with a $750,000 loan could reduce their monthly repayments by $170 when they refinance from an average variable rate of 6.3 per cent to a ‘green’ home loan rate of 5.95 per cent.

Green home loans aim to reward borrowers who invest in sustainable properties.

Aside from reduced interest rates, these types of loans may come with added benefits such as reduced fees, cashback rebates, and the option to borrow additional funding for energy-efficient upgrades.

As long as the property you’ve either purchased, built or recently renovated to be more energy efficient passes the lender’s green home eligibility criteria, and you meet any other loan eligibility requirements, you could be eligible for a green home loan rate.

Who is offering green home loans?

Residential buildings are responsible for around 24 per cent of overall electricity use and more than 10 per cent of total carbon emissions in Australia. The average Australian household emits around 18 tonnes of greenhouse gases annually, with significant contributions from heating, air conditioning, ventilation, appliances, and hot water systems.

Reducing these emissions can be costly, but green home loans help bridge this gap by providing financial incentives for eco-friendly upgrades like solar panels, improved insulation, and energy-efficient appliances.

By making these investments, homeowners not only reduce their environmental impact but also potentially reduce their energy bills and possibly increase their property’s value. That’s a win-win situation.

According to recent research, sustainable properties sell faster and at prices at least 10 per cent higher than non-sustainable ones.

So how do green home loans work?

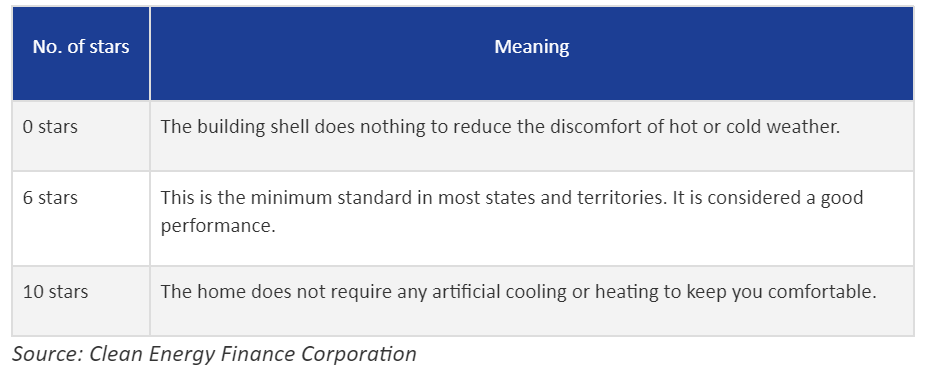

While different lenders will have different qualifying criteria, it is often underpinned by criteria set by the Nationwide House Energy Rating Scheme (NatHERS) and the Clean Energy Finance Corporation (CEFC). To qualify, homes usually need a minimum seven-star rating under NatHERS, which evaluates energy efficiency based on the home’s design. This rating goes up to 10, and a rating of seven is above the average efficiency in most homes today.

Homes may also qualify if renovations improve the energy efficiency rating by at least one star or if the property incorporates features like:

- Solar panels and energy storage systems.

- Battery power and wind power.

- Improved insulation and double-glazing.

- Solar hot water systems.

- Water-saving technologies

In addition to home loans, there are green personal loans and green car loans available for smaller eco-friendly purchases like solar panels and energy-efficient vehicles.

Commonwealth Bank, RACQ, Westpac, and Suncorp offer green personal loans to fund energy efficient home improvements, with rates starting from as low as 2.79 per cent.

But there are pitfalls with green loans.

The criteria for qualifying can be strict, and the loan’s restrictive nature may make switching to a better deal challenging. Additionally, upfront rates and fees can be deceptive, so it’s essential to review the comparison rate and the product disclosure statement to understand the loan’s true cost.

Overall, green home loans are a valuable tool for Australians looking to reduce their environmental impact while saving money. With energy efficiency becoming an increasingly important factor in home buying, and a growing number of lenders offering green loans, the market is expected to become more competitive, making it easier for homeowners to access affordable financing for sustainable upgrades.