Punishing property investors has wider implications for the housing crisis … particularly the rental market.

Rents are rising faster than inflation, so recently I shared some ways tenants can push back.

Now, with the Federal Government considering changes to capital gains tax concessions as part of the housing affordability debate, renters have more to worry about.

The Government says the aim is to improve access to home ownership and reshape incentives in the housing market. But their explanation strikes me as simplistic and doesn’t account for the wider consequences.

I spoke to Ray White chief economist Nerida Consibee about the proposed changes, and she broadly agrees with my stance. She then sent me her research report on what the changes would mean for renters.

Here’s what we think the proposed CGT changes could do to the housing crisis.

Renters will be hit hard

While much of the debate focuses on house prices and investor tax settings, renters – and the rental supply they rely on – have largely been left out of the conversation. Yet renters are currently facing the most acute pressure in the housing system. Investor policy cannot be separated from rental outcomes; the two are directly linked.

If investor participation falls, rental supply tightens. When rental supply tightens, rents rise. The mechanism is straightforward.

Investor behaviour shapes rental supply

Housing markets respond to incentives. Changes to capital gains tax concessions are designed to influence investor behaviour – that is their purpose. But investor behaviour directly affects the amount of rental housing available. Rental housing in Australia exists because investors buy it, and almost every rental property in the country is owned by an investor.

When investor purchases slow, the pipeline of rental stock slows with them. Unlike owner occupiers, who buy to live in a property, investors buy to provide rental housing. If they retreat from the market, fewer properties are added to the rental pool.

At a time when vacancy rates remain tight and rental growth has been strong, any policy discussion that affects investor participation must consider rental supply consequences.

Rental affordability is not separate from investor policy. It is a direct outcome of it.

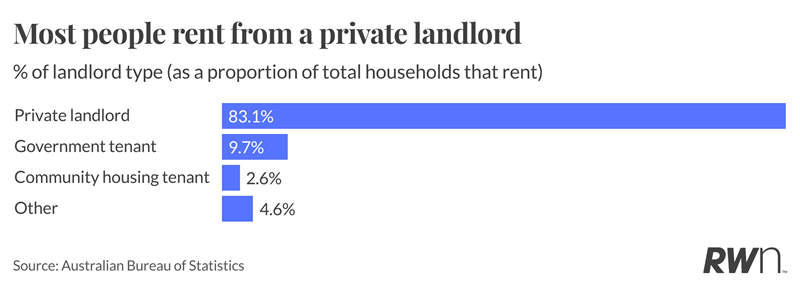

Who provides rental housing?

In policy debates, rental housing is often treated as if it simply exists, rather than being actively provided by someone.

In Australia, that ‘someone’ is overwhelmingly small, private investors, often referred to as ‘mum and dad investors’. These are households who typically own one or two properties, frequently as part of retirement planning.

The data shows that individual investors own the vast majority of rental properties in Australia. Institutional or government ownership remains a very small share of total stock.

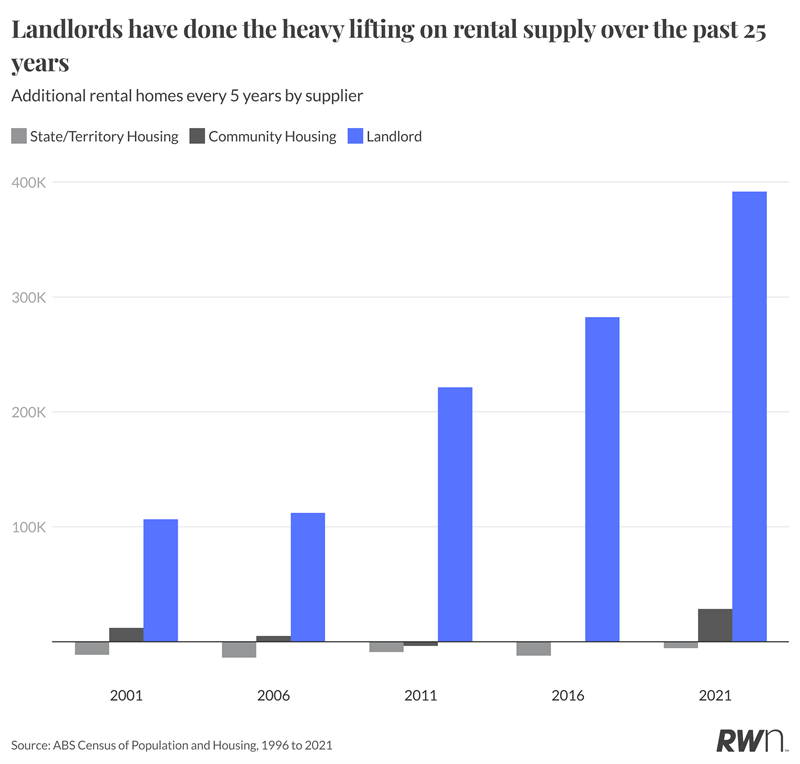

Private investors have also carried most of the burden in expanding rental housing over time.

This structure matters. It means changes to taxation, regulation or holding costs do not affect a marginal group, they affect the core of rental supply.

Lessons from Victoria

Victoria provides a useful example of how investor taxation settings shape housing outcomes.

In recent years, Victorian property investors have become the most heavily taxed in the country. Additional land taxes and other measures have significantly increased holding costs. The impact has been measurable.

Investor participation has fallen and rental listings have declined. As holding costs rise and confidence weakens, some investors exit while fewer new investors enter.

Capital is mobile. When returns are compressed in one jurisdiction, it moves elsewhere — to other states or into different asset classes. The consequence isn’t theoretical: rental supply contracts.

Over the past five years, Melbourne house prices have increased by approximately 20 per cent. Over the same period, rental prices have risen by 34.9 per cent. Rents have significantly outpaced capital growth.

Higher taxes on investors have contributed to slower price growth relative to other markets. From a buyer perspective, that moderation may appear positive. But for renters, the outcome has been very different.

While price growth has been restrained, rental growth has accelerated. Higher holding costs, reduced investor participation and fewer new rental properties have tightened supply. When supply tightens in the context of ongoing population growth, rents rise.

Home owners have experienced slower capital gains while renters have experienced faster rental increases.

Can’t we just build more rental housing?

Build-to-rent is often presented as an alternative to relying on private investors.

Institutional capital funding purpose-built rental housing does have a role to play, and the development pipeline is strengthening.

However, scale and timing matter.

Even with a significant number of projects underway, build-to-rent will account for approximately 0.58 per cent of total rental stock in Melbourne for many years to come, and even less in Sydney.

That is not insignificant in isolation, but it is negligible in the context of total rental demand.

Solving the housing crisis

Housing affordability – for buyers or renters – ultimately comes down to supply.

If population growth continues and housing supply doesn’t keep up, prices and rents rise. And if investor participation slows while rental demand remains strong, rents rise even faster.

Encouraging more investment in new housing, particularly new dwellings, increases rental supply. Discouraging participation reduces it. If the objective is to improve rental affordability, policy must focus on expanding supply.

Watering down CGT concessions will not help the supply shortage.