Like much of the recent media commentary, I’ve pointed out that while the First Home Buyer Guarantee makes it easier for first home buyers to enter the market, it won’t solve the housing crisis. The only real solution is to build more housing. It’s that simple.

If anything, the First Home Guarantee will push up values and further increase demand. Borrowers also need to be careful not to overextend themselves. A lower deposit means a bigger loan and higher interest payments over time.

While this point is widely acknowledged, there’s a side issue missing from the First Home Guarantee conversation:

The rental crisis persists

What much of the media coverage fails to mention is that the extra cost of a larger loan could be offset by what first home buyers save on rent.

Australia isn’t just in a housing crisis, we’re also in a rental crisis. A severe shortage of rental properties has pushed up rents, becoming a major driver of inflation.

Taking advantage of the First Home Guarantee gives young Australians the opportunity to swap rent payments for a place of their own. While it does involve taking on a significant loan, home ownership offers the benefit of investing in an appreciating asset and building equity over time.

Property research group Cotality has crunched the numbers on rent vs loan repayments. And the outcome is compelling.

Rent vs mortgage

Since the First Home Loan Deposit Scheme was introduced in January 2020, rent costs have soared. As of January 2020, the median weekly rent across Australian dwellings has increased by about $200, reaching $669 a week – an uplift of over $10,000 a year.

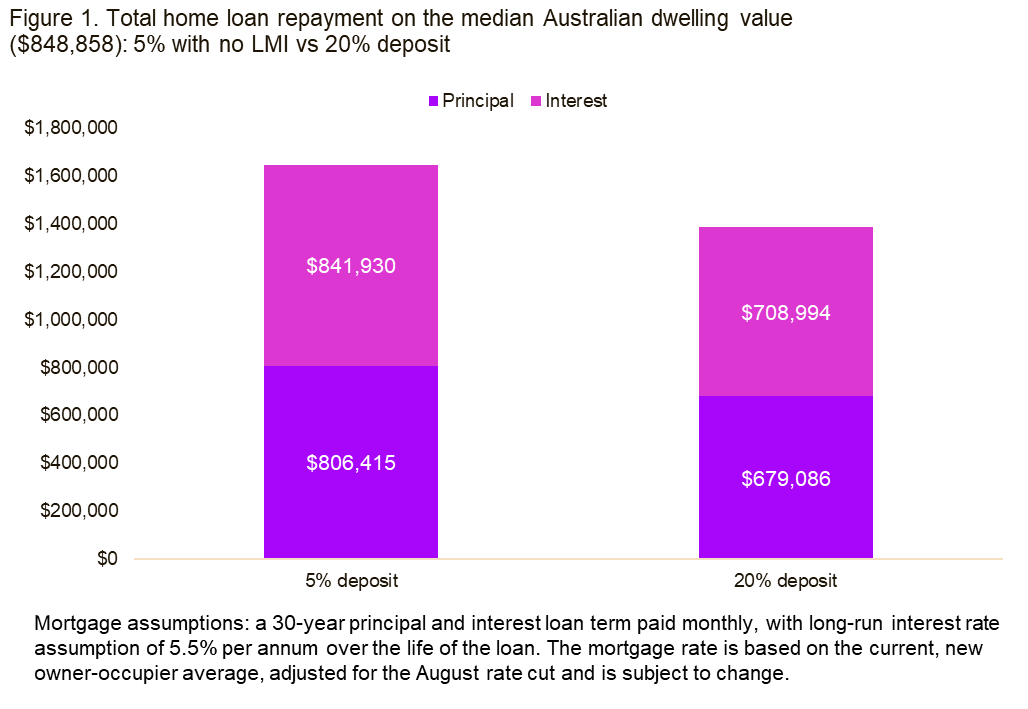

According to Cotality, First Home Guarantee schemes do come with costs both for individuals and the broader housing system. The main cost for buyers is the higher interest paid over the life of the loan. A 5 per cent deposit means a 95 per cent loan-to-value ratio, which results in more debt and more interest compared to a traditional 20 per cent deposit. The chart below shows this impact using Australia’s median dwelling value as an example.

Over a 30-year loan, the additional interest can amount to tens or even hundreds of thousands of dollars compared to a 20 per cent deposit loan.

Even so, a smaller deposit and higher interest might still work out cheaper for renters. Entering the market sooner could mean spending less time paying rent, and those savings add up.

Big rental saving

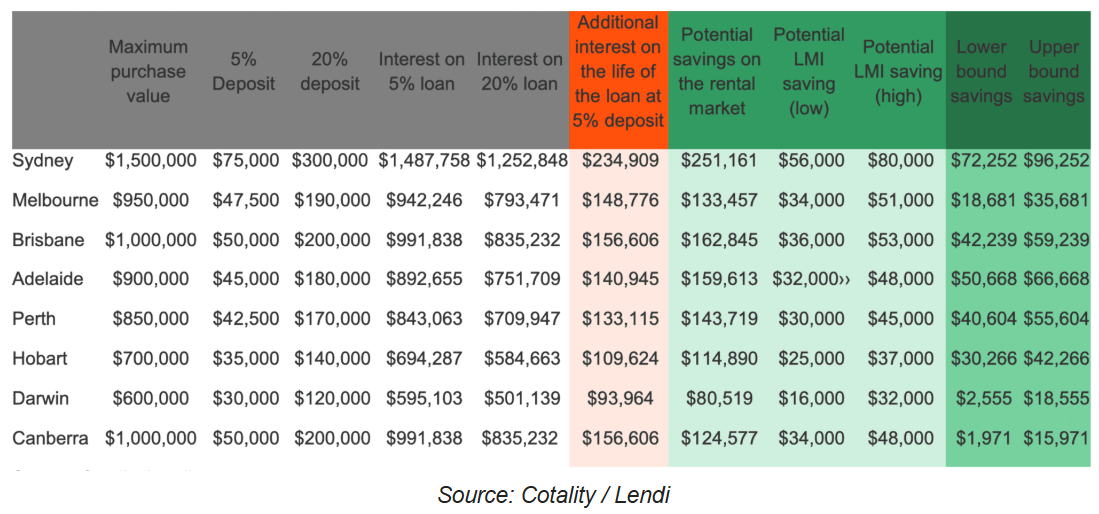

The biggest savings across the capital cities are estimated to be in Sydney, where a 5 per cent deposit could reduce the time needed to save for a home deposit by around six years and save roughly $251,000 in rent, based on a weekly rent of $801.

The table below compares the additional interest cost of a 5 per cent deposit with potential Lenders Mortgage Insurance (LMI) and rental savings.

In this case, buying sooner through the scheme is more financially favourable than renting longer to save a full deposit. In fact, rental savings far outweigh LMI savings.

In this case, buying sooner through the scheme is more financially favourable than renting longer to save a full deposit. In fact, rental savings far outweigh LMI savings.

According to Cotality, someone not paying rent may still be better off saving the full 20 per cent deposit – avoiding both LMI and extra interest. But even non-renters must weigh the benefit of getting into the market earlier, especially with prices still rising.

Housing supply still the biggest issue

Getting a foot on the property ladder sooner is also a smart move with no clear solution to Australia’s housing supply shortage in sight.

August building approvals show that government initiatives are falling short. The total number of dwellings approved fell 6 per cent in August to a 12-month low. Approvals are up just 3 per cent year-on-year, which is the weakest annual growth since June 2024.

Council consents for private houses also dropped 2.6 per cent to an eight-month low of 9,027, while apartment approvals fell 8.1 per cent to a four-month low of 5,408.

The annualised rate of building approvals rose to 187,691 in August – the highest since January 2023 – but remains well below the federal government’s target of 240,000 homes per year.

The federal government’s goal of 1.2 million new homes by 2029 looks increasingly out of reach.

On the upside

While the First Home Buyer Guarantee won’t fix housing supply and in fact fuel demand, it can still help some. Those who are able to save the 5 per cent deposit could shift from paying off someone else’s loan to building equity in their own home.

So while much of the debate focuses on whether the scheme inflates the market or burdens buyers with bigger loans, we should also look sideways:

Australia’s rental crisis, caused by the same supply issues, could be avoided by those who manage to get a foot in the door with a lower deposit (which is hard, I know).

But the government absolutely needs to solve the housing supply issue – it’s the only way to properly address the housing crisis.