I’ve talked a lot about the housing shortage and why it’s pushing property values up so much, but I was fascinated to read a great report from Cotality head of research, Eliza Owen, on the issue.

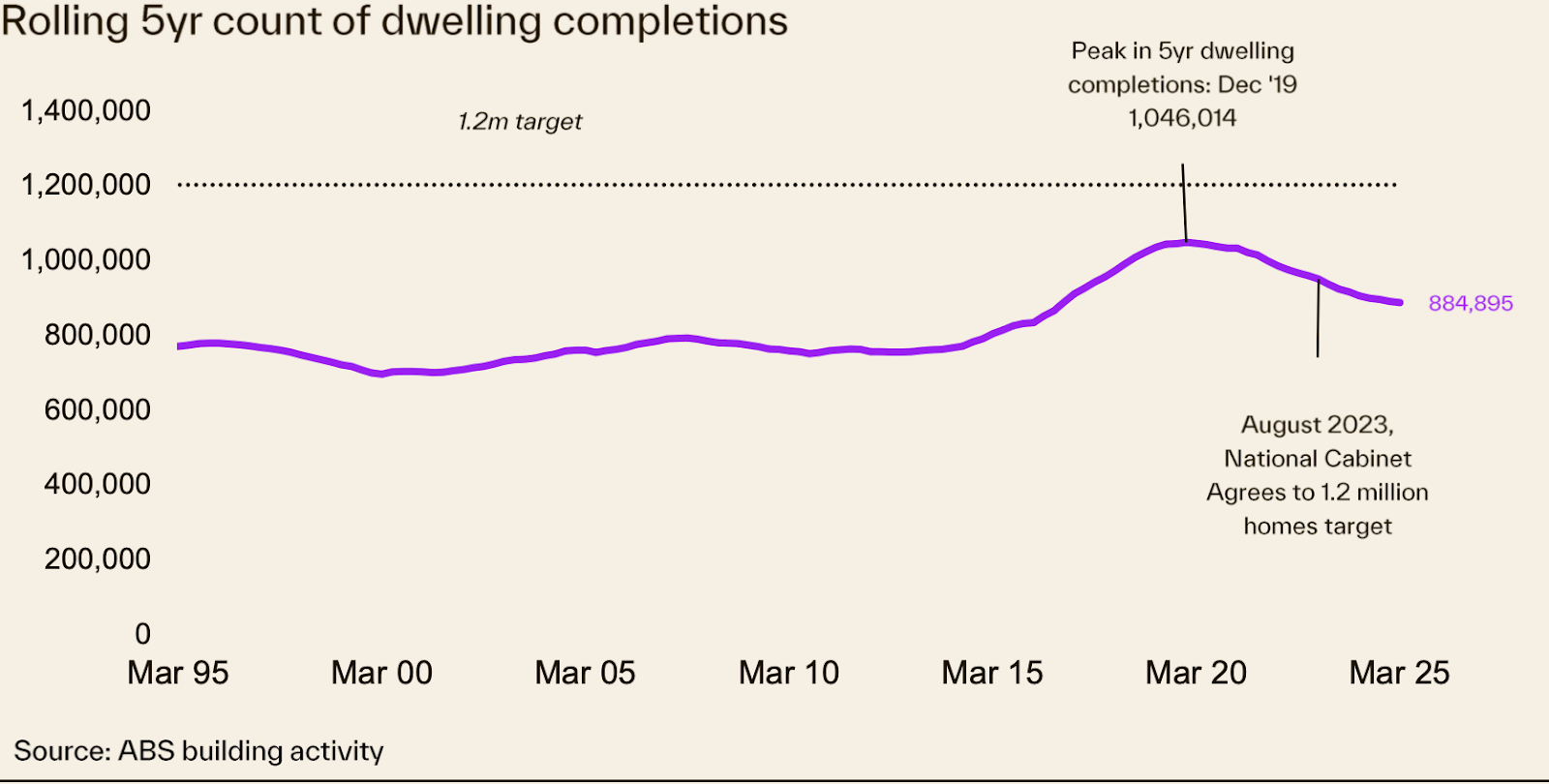

Eliza reminds us of the target National Cabinet announced in August 2023 to build 1.2 million new homes in five years. It was an announcement that was met with a lot of scepticism as the problem with any government target for new dwellings is that the government can’t influence many of the factors that determine demand and supply.

How did we go?

While state and local governments focus on approvals and improving the feasibility of new projects, building companies continue to be stretched thin across an already swollen pipeline and reducing margins.

The closest Australia came to 1.2 million dwelling completions over five years was at the end of 2019 – under very different market conditions:

The cash rate averaged just 1.6 per cent, compared to 4.18 per cent since July 2024.

Units made up 46 per cent of approvals in the five years to 2019, versus just 37 per cent in the past five years, making dwelling completion more scalable.

Investor demand was stronger, supporting off-the-plan apartment pre-sales. ABS data shows investors peaked at 44.8 per cent of new housing finance nationally in the June quarter of 2015, and 55 per cent in NSW.

Foreign investment in new residential properties was higher, with NAB reporting foreign buyer purchasers of new homes holding above 10 per cent through much of the 2010s.

But Eliza points out that despite that building boom, home ownership rates fell, apartment value growth was poor and the level of defects in these homes was high.

Government can’t control markets

Over the last few years, lending is more prudent, build quality is better, and new apartments are larger and geared towards owner-occupiers.

To move the dial on the numbers, state and local governments have enacted changes to speed up planning and approval processes and increase new home purchases.

Despite these changes, dwelling approvals have generally remained very low. Why?

Eliza believes it is in part because of relatively high interest rates, affordability constraints, and new purchases being brought forward under the HomeBuilder Scheme (which was overlaid with other incentives such as the then recently introduced First Home Guarantee).

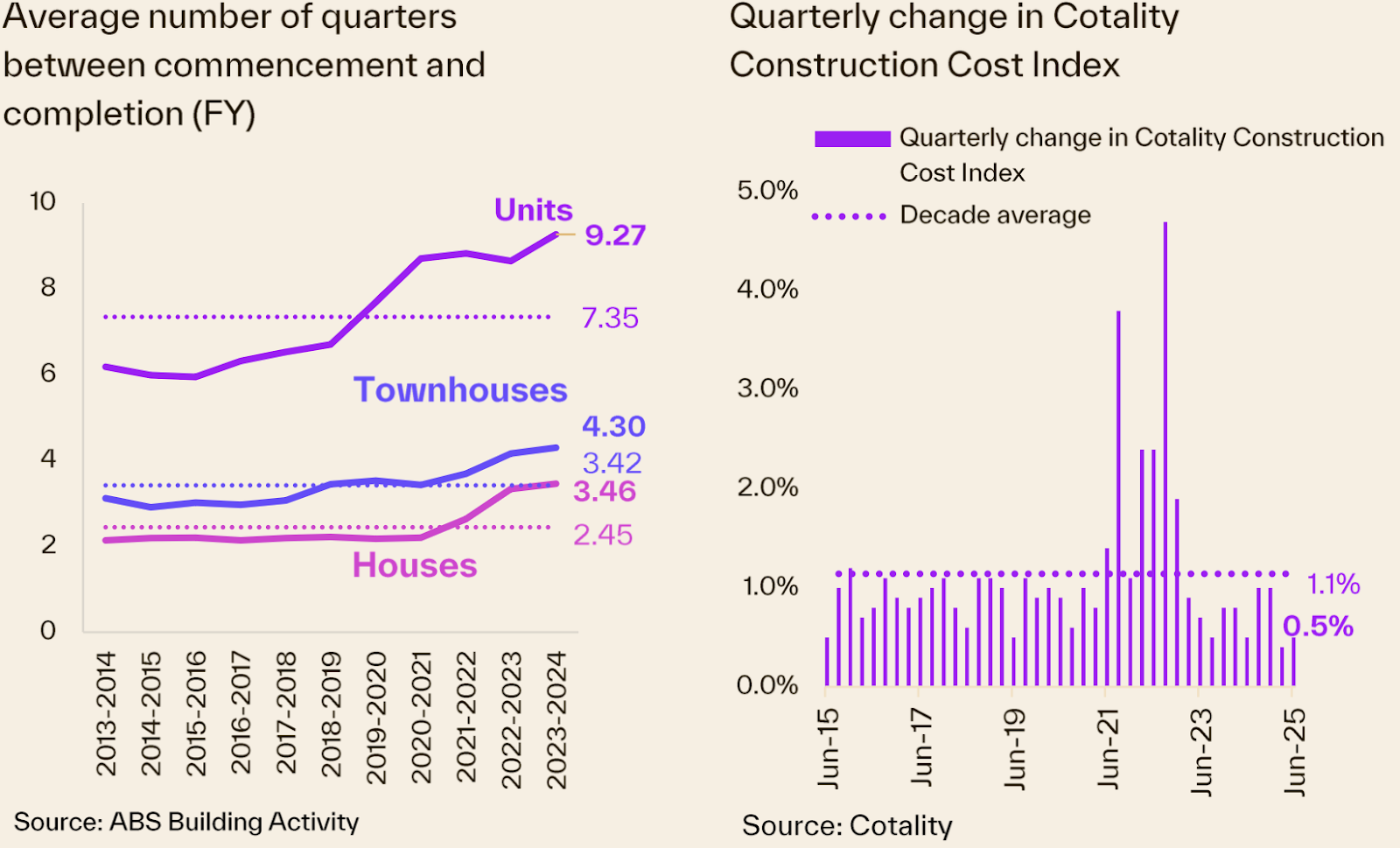

Buyers may also be lacking confidence in new builds following a surge in construction costs between 2021 and 2023. Total dwellings approved averaged 15,611 per month over the year to June, down from the decade average of 16,770, and well below the average 20,000 needed for 1.2 million homes in five years.

State and local governments can influence dwelling approvals, but interest rates are an extremely important factor as to whether there is market demand for new housing and whether developers will seek approval for new projects. Unit approvals are averaging about 7,000 a month, but this is well below the 13,000 peak found through the more favourable market conditions of the 2010s.

A building bottle neck

Eliza is hopeful that building approvals could move higher in the coming months, as recent zoning reforms and incentives for new builds at the state level coincide with falling interest rates. But this could present a problem for the construction industry: it may add more new projects to an already swollen pipeline. It’s like turning up the tap on a bath that is already full.

Building activity data from the ABS shows there were just over 219,000 dwellings under construction in the March quarter of 2025, and a further 30,000 dwellings that have been approved, but have not yet commenced construction.

Effectively, dwellings are being approved but getting ‘stuck’ in the commencement and construction phase.

With completion times already above average, and construction costs elevated, Eliza believes it’s an odd time to be incentivising more dwelling approvals and commencements to the backlog of work to be done. In fact, without increasing the capacity or productivity within the construction sector to take on this additional work, it could even present an upside risk to inflation, at a time when the industry is crying out for rates to move lower.

Reducing demand

Productivity in the building industry is being questioned with the Productivity Commission estimating a 12 per cent decline over the last 30 years. Making homes faster and cheaper to build, while still maintaining quality, resilient homes is the key challenge for policymakers to focus on right now.

Winding back negative gearing and capital gains tax concessions for residential property, implementing broad-based land taxes or including the family home in the pension asset test are all examples of policies that could reduce demand for housing, and potentially the need for as much new supply altogether.

This would have the added benefit of easing capacity in new home construction, rather than risking more inflationary pressures for new housing construction.

All eyes now turn to the National Productivity Summit, where leaders across government, industry and unions will debate the very reforms that could reshape elements of both supply and demand.

Eliza says, if governments are serious about delivering 1.2 million homes, they must focus on building capacity, lifting productivity, and ensuring every approved home actually gets built.