Protect your wealth from the blow of another rate rise with these simple tips to decrease your mortgage and pay it off quicker.

How would another rate hike impact your household budget? A single 0.25 per cent increase could add around $123 to monthly repayments on a $750,000 mortgage. That could be $1,400 more over the course of a year if rates don’t budge thereafter.

So how can you put yourself in a better position to ride out a possible hike and improve your budget for the long term?

Here are my top three mortgage hacks to pay off your loan faster and potentially soften the blow of future hikes over time.

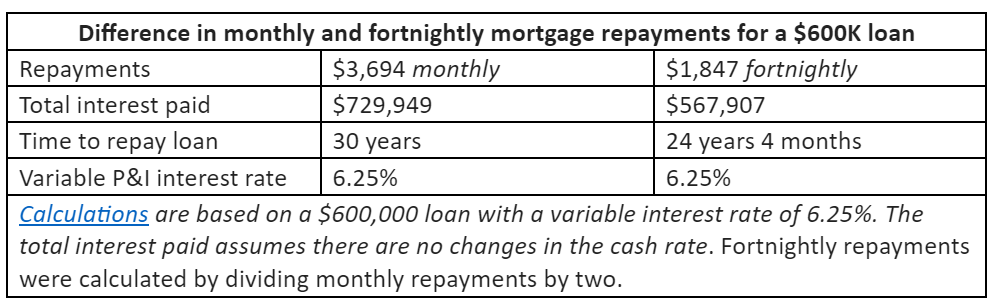

1. Switch to fortnightly repayments

By making a small change to their repayments, homeowners could save tens of thousands of dollars and pay off their loans faster.

Compare The Market crunched the numbers and found a person with a $600,000 loan could save over $160,000 in interest over the life of the loan (and cut down their loan term by over five years) if they were to switch to fortnightly payments instead of monthly.

You’re not just paying slightly more, you’re paying it back early.

But you’ll need to tell your bank that you want to pay half of your monthly repayments fortnightly. Because if you simply switch to a fortnightly repayment plan, this could be a smaller payment amount, and then this hack might not work for you.

For example, if your monthly payments are $3,694 you will want to pay $1,847 per fortnight. Because of the calendar, this means you’ll be paying an extra $3,694 each year, which will cut down your principal and interest owed to the bank.

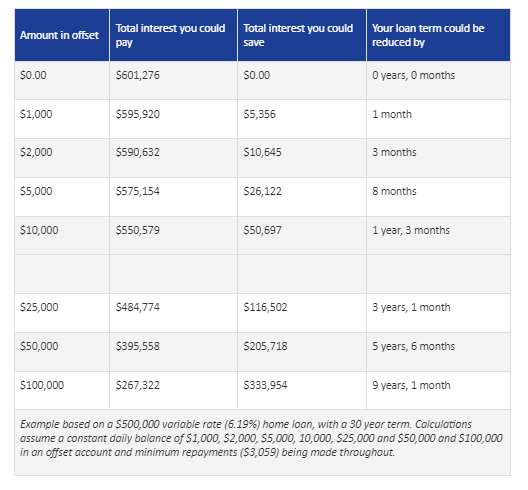

2. Put savings into an offset account or make extra repayments

If you keep a decent balance, an offset account has the potential to help you save money in loan interest and pay off your mortgage sooner.

It’s also a great incentive to save. And unlike regular savings accounts, you won’t pay tax on the interest you offset.

Having just $25,000 in an offset account for a $500,000 loan with an interest rate of 6.19 per cent could reduce your loan term by three years and 1 month and save more than $110,000 in interest over the life of the loan.

If you want to shrink your loan size immediately, you may consider just making extra repayments. Improving your LVR (Loan to Value) may help you to access more competitive rates.

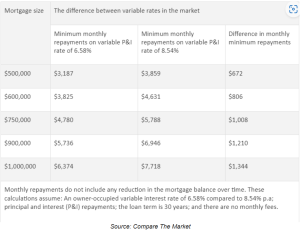

3. Refinance to a better rate and adjust your loan term

Borrowers shouldn’t wait for a cut in the cash rate. A Compare The Market analysis of some of the rates available from the Big Four showed the average difference between front-book (new customer) and back-book (existing customer) rates is 1.96 per cent.

Therefore, a person with an owner-occupier $750,000 loan could be saving $1,008 a month if they switch from a rate of 8.54 per cent to 6.58 per cent.

I’d encourage people to be sceptical of their home loan interest rate and to compare it against what their lender and other lenders are offering new customers. If you’ve been with your lender for more than a couple years, there’s a good chance you’ve fallen on a higher ‘back book’ rate and are paying more than you need to be.

If you can, adjust your loan term to reflect your mortgage journey status and repayment goals. If you choose to retain a 30-year loan, your monthly repayments will be smaller, but you will end up paying much more in interest over time.