School is supposed to equip our kids for life, and yet financial literacy is not a compulsory subject. Is it tine we changed the school curriculum to include it?

It is a common concern that Aussie kids aren’t learning anywhere near enough about personal finances, with most Aussies receiving little to no money education at school.

In today’s difficult economic climate, knowing some budgeting basics could be the difference between saving for life’s small pleasures and sliding headfirst into debt.

And for a long time, we’ve been told that it’s a parent’s responsibility to teach their children about finances. But times have changed.

While parents still play a key role in transferring financial attitudes, behaviours and knowledge to their children, many people feel the school curriculum could be improved.

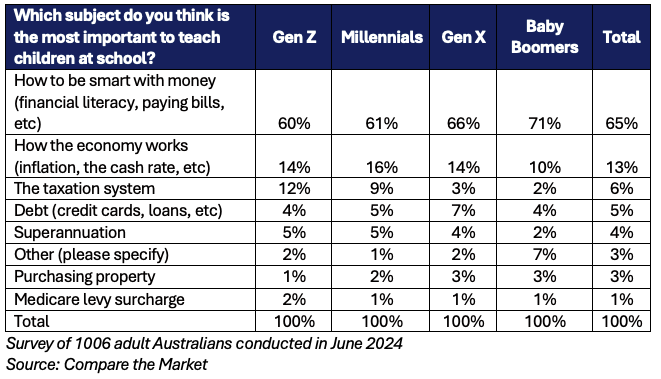

A recent Compare the Market survey revealed that 65 per cent of people said that ‘how to be smart with money’ is the most important topic that should be taught in school. This was followed by how the economy works (13 per cent), the taxation system (6 per cent), and debt (5 per cent).

Nowadays, it’s rare for one parent to work while the other stays at home to raise their kids. The rising cost of living has made it nearly impossible to survive on one income. In Australia, both parents often work full-time jobs to support their family. This means they would only have weeknights, weekends, and holidays to teach their kids about money.

Remember though that children adopt their financial habits from observing their parents. So, we all have to set a good example in this area.

But more than 95 per cent of Australians believe children should receive greater education about managing personal finances and budgeting during school.

In the same survey, a startling 18 per cent of respondents said they were never spoken to about money, and 29 per cent said they were rarely spoken to about money. Meanwhile, over a third of people said they were sometimes spoken to about money (34 per cent). Just 19 per cent said their parents spoke to them often about money.

The thing is, money used to be such a taboo topic no one spoke about how much they earned or what their money goals were (if they had any).

Although it’s improved with the rise of the digital age and access to information, there’s still a lot of work to do to improve financial literacy.

According to a study from the University of Western Australia, 8.5 million Australians – 45 per cent of the adult population – don’t understand at least three basic financial literacy concepts: interest rates (especially compounding interest), inflation and diversification.

These basic financial topics affect everyone, yet none of them are taught in school unless you opt into an economics subject.

What can the government do?

A number of advocates, including the Ecstra Foundation and Your Financial Wellness group, have recommended the government reactivate the National Financial Capability Strategy.

This strategy used to be run by the consumer regulator ASIC, and has been recently transferred to the Federal Treasury, but we haven’t heard anything since 2022.

Treasury should make financial literacy a compulsory unit in the school curriculum. Students need to be taught ways to manage their personal finances, budgeting, how to pay bills and the importance of saving money.

While it may seem like common sense to some, there’s a reason why Buy Now, Pay Later services have taken off. People don’t want to save up and wait for their reward, they want it now.

Which is exactly why Buy Now, Pay Later services, just like credit cards or loans, should be spoken about in school as well. These are all essential life skills that many of us have had to learn on the go and, unfortunately, some people have suffered financially because of their lack of financial knowledge.

The government needs to commit to a national strategy that will provide funding for developing financial literacy and investigate where we have previously gone wrong.

Financial illiteracy can lead to debt, poor credit, bankruptcy, housing foreclosure and other negative consequences.

However, financial illiteracy doesn’t just affect individuals; it also increases the financial risk to the economy… which is precisely why the Treasury should be concerned.