Global private credit has emerged as the not-so-quiet achiever for everyday investors looking to diversify their investments and achieve more reliable returns without share market shocks.

Long favoured by big super funds, institutional investors and the mega-rich, global private credit is now available for everyday Australian investors hunting the promise of steady monthly income at a lower volatility level than equities and listed fixed income.

Private credit is an asset class where investors lend money at a higher interest rate than, say, a term deposit, and see higher returns. (Note: private lenders are not banks – private credit refers to ‘non-bank’ lending).

Globally, the private credit market is huge. In fact, right under our noses, global private credit has become the world’s fastest-growing asset class over the past 15 years.

“It’s a massive, mature, and highly appealing asset class that, to date, simply hasn’t been available to Australian investors,” explains Dean Weinbren, an executive director at ASX-listed investment firm Pengana Capital Group.

“The meteoric growth of global private credit as an asset class has largely been due to the historical track record of resilience that it has shown versus other fixed income asset classes across economic environments and time periods.”

In Australia, investment firms like Pengana are seeking to democratise access to the global sector with offerings like TermPlus, an online term account platform delivering monthly income returns underpinned by a diversified portfolio of global private credit. TermPlus offers floating target returns with a fixed margin above the RBA Cash Rate, starting at 7.10 per cent per annum (for a one-year term account, at the time of publishing).

Global private credit is especially attractive to people with an appetite for lower risk in exchange for potentially higher returns and a fixed monthly income, without having to ride the roller coaster of the share market. It may also be seen as a complementary investment strategy to diversify returns alongside other asset classes.

But before you go any further, here’s a bit of a global private credit 101.

What is global private credit?

Private credit is a form of lending outside of traditional banks and public debt markets, where non-bank lenders, like investment firms and asset managers, negotiate loans directly with borrowers. For example, there are vast numbers of corporate loans for businesses in the USA and Europe with yearly earnings of US$50-$250 million – yes, we’re talking about billion-dollar valuation companies that may require extra funding for special projects, acquisitions, expansion, infrastructure and more.

In short, private credit has filled a gap left by the US and European banks after they pulled back on lending post-GFC. At the same time, investors have been hunting for alternative means to achieve high returns. Bringing supply and demand together, private credit answers investor demands for diversification, steady income and better risk management – big pluses for institutional investors like pension funds, and now available for everyday investors.

“The ability of private credit lenders to offer bespoke solutions to established mid-market companies, that are not large enough to access public debt markets, allows them to charge a premium without incurring additional risk,” says Weinbren.

“Investors are able to tap into the attractive and reliable returns offered by the global private credit sector, which also add an additional layer of diversification to portfolios.”

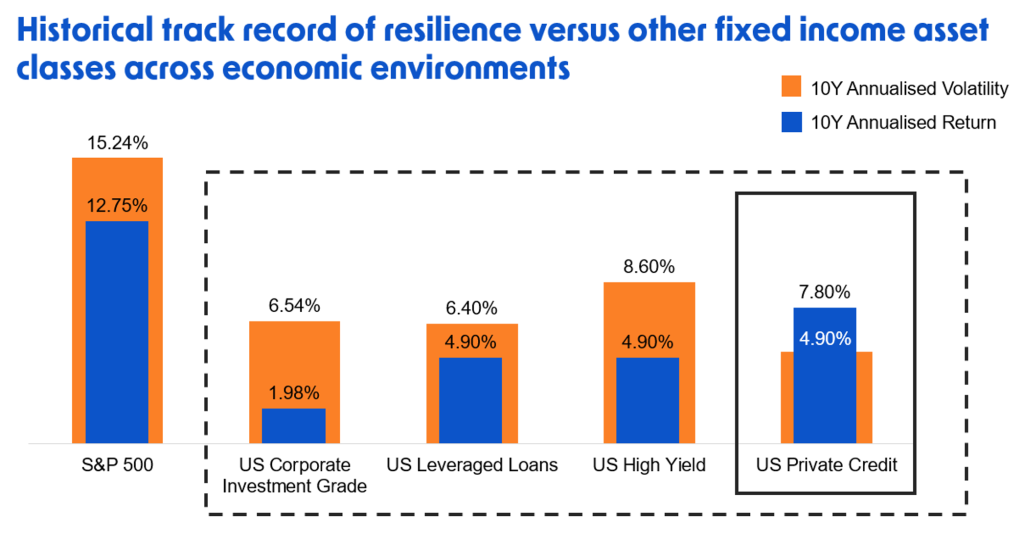

Global private credit has shown higher annual historical returns than other growth fixed income asset classes at lower volatility levels, as this chart comparing US private credit with other US fixed income asset classes shows:

Returns in USD, 10-year period ending 30 September 2024. Sources: S&P (S&P 500 Total Return Index), Bloomberg (Bloomberg US Corporate Total Return Value Unhedged USD), Burgiss (Source: Private Debt, North America) and Thomson Reuters Datastream (ICE BofAML, US High Yield Master II, S&P Leveraged Loan). S&P, Bloomberg, Burgiss and Thomsen Reuters have not provided consent to the inclusion of statements utilising their data. No assurance can be given that any investment will achieve its objectives or avoid losses. Past performance is not necessarily a guide to future performance. Volatility refers to “Annualised Standard Deviation”, a measure of how much the price of an asset or the return of a portfolio of assets has fluctuated (both up and down) over a certain period. If an asset or portfolio of assets has a high Annualised Standard Deviation, the price of the asset or portfolio of assets has historically fluctuated vigorously. If an asset or portfolio of assets has a low Annualised Standard Deviation, the price of the asset or return of the portfolio of assets has historically moved at a steady pace over a period of time. Image: Pengana Capital Group.

How big is global private credit?

According to alternative assets researcher Prequin, global private credit is estimated to nearly double in size to US$2.8 trillion by the end of 2028. While the Australian private credit market is a very small piece of that pie, the global private credit market itself is a very big pie indeed.

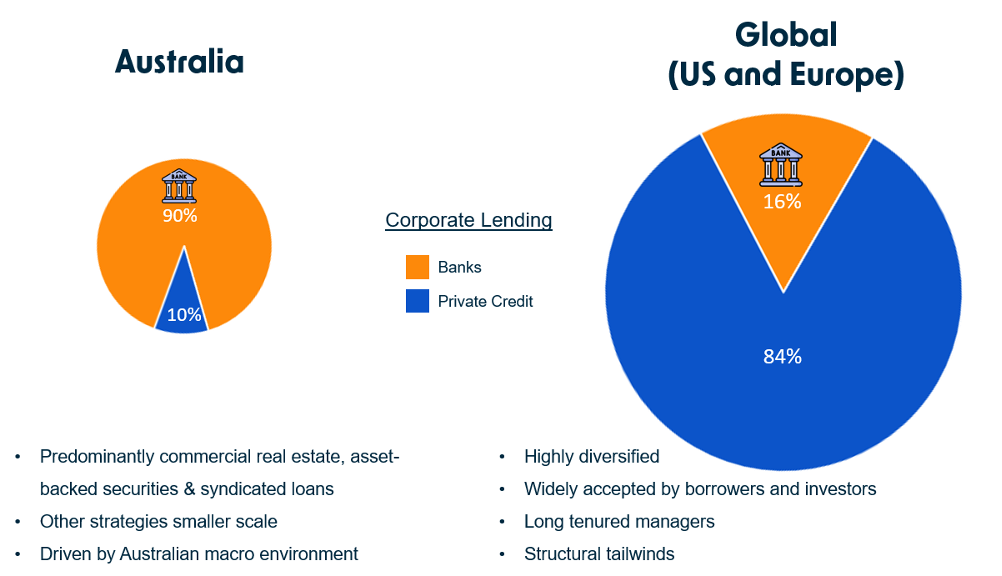

As you can see below, only 10 per cent of corporate lending in Australia is private credit. In the global private credit scene – US and Europe – that number is 84 per cent.

The Australian private credit market versus the global private credit market. Image: Pengana Capital Group.

This poses an opportunity for Australian investors. Think of how 15 or 20 years ago, investing in big US tech stocks was barely on the radar for a retail investor. Now, it’s an everyday part of millions of Australians’ investment portfolios.

The same could soon be true for global private credit, with local fund managers eroding traditional barriers to entry.

There’s no longer high minimum investment amounts – TermPlus investments start from $2000 – and online access to specialised term accounts is becoming as simple as any other online account.

Case in point: TermPlus

Pengana, which has been building differentiated investment products for Australian investors for 23 years, offers investors a global private credit portfolio made up of more than 2000 individual contractual loans to companies in the US and Europe, in partnership with investment consultant Mercer.

When you invest in a TermPlus account, you are investing across those underlying loans, benefiting from the associated contractual protections and returns, says Weinbren.

“With an established and seeded portfolio already in place, we built a 100 per cent customised online term account product with a diverse feature set and inbuilt layers of customer account protections in order to provide attractive and reliable returns, whilst focussing on reliability of income and stability of capital for TermPlus account holders,” he says.

Since its launch in early-2024, TermPlus has paid 100 per cent of targeted income rates, Weinbren adds. This means that investors have consistently received monthly income equivalent to the RBA Cash Rate plus an additional 3 per cent per annum if it’s a one-year account (RBA Cash Rate of 4.10 per cent at the time of this article’s publishing, plus 3 per cent, for a total 7.10% p.a. return), 3.65 per cent per annum for a two-year account (currently a total 7.75% p.a. return), and 4.15 per cent per annum for a five-year account (currently a total 8.25% p.a. return).

While this is one example, it’s always important to speak to your financial adviser to check that products like TermPlus fit your investment strategy.

How risky is private credit?

First, every investment has a level of risk involved. Global private credit is historically less volatile than equity market investments, but is a different investment product with its own risk matrix. Here are some features of private credit products:

- Credit investors are prioritised in the capital structure, meaning they are paid before equity holders in the event of a company’s liquidation or bankruptcy.

- Private credit investments offer fixed interest payments, paid on a monthly basis, secured by assets like real estate and equipment, which investment firms say provides a strong buffer for lenders.

- While equity markets can be a white-knuckle ride of share market ups and downs, global private credit marks have shown to be less volatile and offers the promise of more predictable returns in comparison.

- There are rigorous contractual protections and due diligence processes in place.

- They have historically lower default rates on loans when compared to other high-yield asset classes, and have displayed higher recovery rates compared to equity.

“Overall, global private credit offers more stability and lower risk because of its structured nature, legal protections, and priority over equity in the event of financial distress,” says Weinbren.

Like any product though, the fund you invest in requires careful thought and research. As the private credit sector continues to grow, so do the needs for greater transparency and governance – areas that regulators APRA and ASIC are currently keeping a close eye on.

Speaking to a financial adviser to understand how you’ll make up the pieces of your investment pie can ultimately help determine whether private credit is for you.

Find out more about TermPlus at termplus.com.au.

This article is brought to you by Your Money & Your Life in partnership with TermPlus.

Feature image: AdobeStock

Disclaimer: Pengana Capital Limited (Pengana) (ABN 30 103 800 568, AFSL 226 566) is the issuer of units (Term Accounts) in TermPlus (ARSN 668 902 323). Any advice provided is general in nature and does not take into account your particular objectives, financial situation or needs. You should consider the PDS and TMD before investing in TermPlus.

Any reference to a target rate is a reference to the investment objective for the relevant account option in TermPlus, which may vary. Importantly, target rates are not guaranteed, and any investment is subject to investment risks. Any forecasted returns may not reflect actual performance and past performance is not a reliable indicator of future performance.

Pengana is not a bank and is not regulated by the Australian Prudential Regulation Authority. Investing in TermPlus is not the same as depositing money with a bank. For further details, please see the Important Information page on the TermPlus website.

Mercer Consulting (Australia) Pty Limited (ABN 55 153 168 140, AFSL 411 770), which is a wholly owned subsidiary of Mercer (Australia) Pty Ltd (ABN 32 005 315 917) (Mercer Australia) collectively referred to as Mercer. References to Mercer shall be construed to include Mercer LLC and/or its associated companies. ‘MERCER’ is a registered trademark of Mercer Australia.