Australians have the highest proportion of variable home loans in the world, but is it time to switch to a fixed rate home loan, or have a cocktail of fixed and variable?

I know that sounds crazy when there is huge anticipation for a cut in interest rates from the Reserve Bank on the horizon. But given the difference between variable and fixed rates, plus a growing doubt about the timing and size of a future cut, fixing could be a consideration.

In last week’s RBA board minutes, it was made clear that there would be no rate cut until two consecutive quarterly CPI results landed within the 2-3 per cent target range.

Strip the ‘headline rate’ artificial sweeteners out (such as government rebates) and the trimmed mean CPI actually rose for the month from 3.2 per cent to 3.5 per cent. So, through the eyes of the RBA, inflation is getting worse rather than better using its filter.

If you assume the September quarter CPI was not a good result in the eyes of the RBA, it would need a good result in the December and March quarters before it would consider cutting rates. The March quarter CPI result is released on 20 April and the RBA meets on 19-20 May next year – after the 17 May deadline for the federal election.

There is a very good chance we won’t get a rate cut before the next election even if it is held late. That’s why the Federal Treasurer is getting so aggressive in spouting the Government’s economic credentials.

Looking at the rate horizon

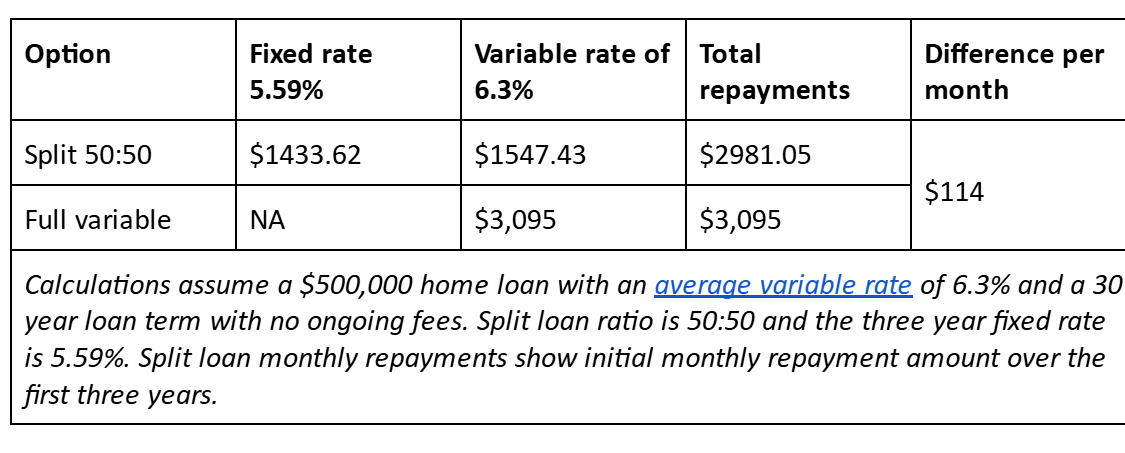

Let’s assume there is no rate cut until at least May, which is almost six months away. Currently the average variable home loan rate is 6.3 per cent, but there are some two and three year fixed rates as low as 5.59 per cent – that’s almost a 0.75 per cent difference, or three RBA cuts.

Analysis by comparison website Compare the Market shows a borrower with a $500,000 split loan could potentially reduce their repayments by $4,104 over the first three years if the cash rate were to remain unchanged.

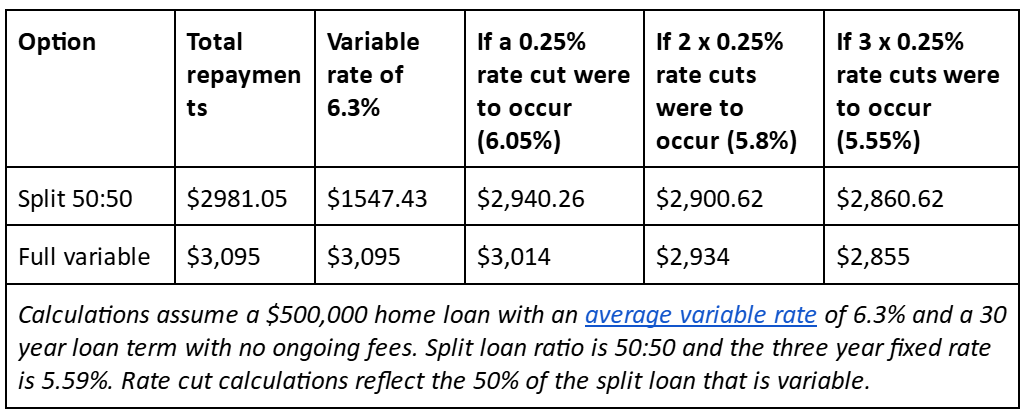

Even if the Reserve Bank were to drop the cash rate twice by a total of 0.50 per cent, borrowers would continue to pay less on their fixed portion at a rate of 5.59 per cent. Only after a third 0.25 per cent rate cut would the average variable rate beat the split loan option for savings.

Source: Compare the Market

Source: Compare the Market

The reality is, we don’t know if, or when, rates will drop but it’s hard to find variable rates below 6 per cent.

Interest rate forecasting has become a financial sport and there are plenty of experts who have egg on their faces at the moment. Remember six months ago when the major banks were predicting at least one, maybe two, interest rate cuts by the end of 2024? Hasn’t happened.

What about inflation?

Inflation hasn’t slowed as expected thanks to a combination of rent, building costs, insurance premiums and wage rises feeding into the services sector. These are the “sticky” cost increases holding up the inflation rate and holding up the RBA from rate cuts.

Now with the US election of President Donald Trump and his inflation-boosting policies (increasing tariffs and mass deportations of illegal immigrants), there is a fear we will see a spike in US inflation. This could be exported overseas and the Federal Reserve will need to curtail future rate cuts.

Splitting your home loan

This increasingly uncertain inflation and interest rate outlook is why the difference between variable and fixed rate home loans is interesting.

A hybrid approach allows borrowers to hedge their bets and experience the benefits of both rate types. Just remember you’re also exposed to the risks.

Fixed rates are great for shielding you from rate rises, but if the cash rate happens to fall, you may miss out on savings.

Split loan pros:

- Interest rate security – This stability can be reassuring for families and individuals on a budget who need to manage their monthly expenses, without surprises.

- Flexibility of a variable rate – If interest rates drop, borrowers will see lower payments on this portion of the loan, allowing them to take advantage of the market’s fluctuations.

- Extra repayment options – Most variable-rate loans allow additional repayments without penalty, and the variable portion of a split loan is no exception.

- Balanced risk approach – Borrowers can shield part of their loan from interest rate hikes while still being open to benefits if rates drop. This diversification of interest rate exposure is particularly appealing to those who want to avoid committing entirely to a fixed or variable rate.

Split loan cons

- Fluctuating repayments – If a portion of your home loan is variable, your monthly repayments might change if interest rates vary. This could make budgeting harder.

- Interest rate changes – If interest rates increase, your variable loan portion will increase. Conversely, an interest rate drop might mean you don’t fully benefit if your fixed rate portion remains steady.

- Fees – Lenders charge fees and having two loan products could result in different fees. Some loans also have break fees if you want to leave a loan early.

Choosing a split loan depends on individual needs, circumstances, financial goals, and risk tolerance. Before making any decision, I’d encourage prospective borrowers to talk to a home loan specialist to better understand their options.