With a rate cute and potentially more on the horizon, how can you make the most of it? Here’s what I think …

A 0.25 per cent cut in interest rates wasn’t a big surprise to me at the recent Reserve Bank board meeting. What was, howver, is that they debated a 0.5 per cent cut.

RBA Governor, Michele Bullock, dropped this tidbit during her press conference following the decision. But the board ultimately decided there was no overwhelming reason to go for the “double cut”.

It does, though, give an insight into the psychology of the board and how comfortable they are now inflation is back down to within their 2-3 per cent target range.

More cuts on the way?

The cash rate now sits at 3.85 per cent, after the two most recent cuts which the RBA described in its statement as, “Monetary policy somewhat less restrictive,” with the March quarter CPI data providing them with, “further evidence that inflation continues to ease.”

Trade wars driven by the US are still top of the RBA’s list of worries: “This has also contributed to a weaker outlook for growth, employment and inflation in Australia,” the board stated.

The RBA still considers the labour market to be “tight”, meaning there are more jobs than workers available. However, it has slightly lowered its expectations for how fast wages will grow, and it now expects the unemployment rate to rise a bit higher – peaking at 4.3 per cent in December 2025, up from a previous forecast of 4.2 per cent.

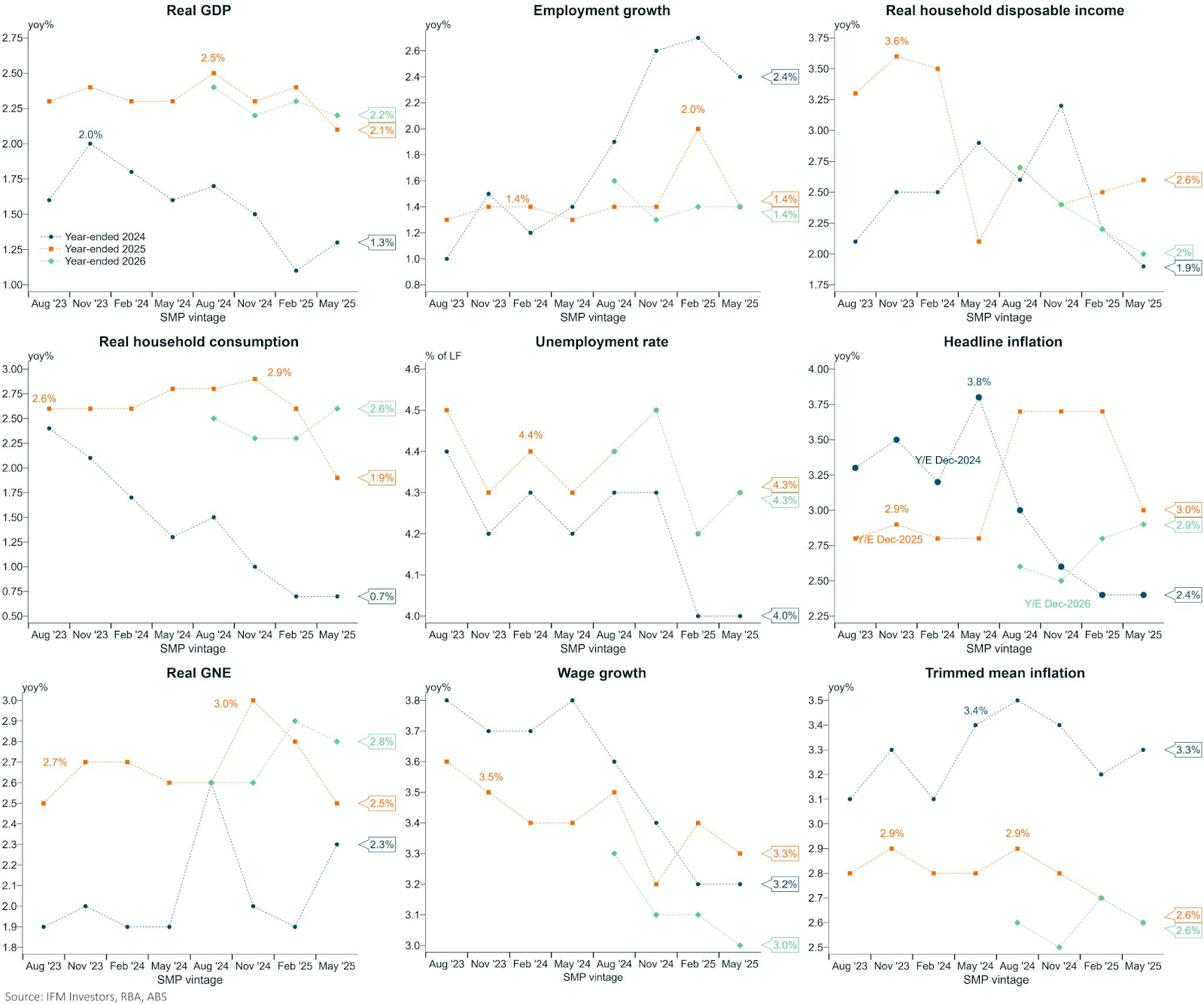

Continuing weak consumer demand has also prompted the RBA to downgrade its forecast for economic growth from 2.4 per cent previously, to now 2.1 per cent. That’s a pretty big slowdown from what was expected.

This chart shows all the RBA forecasts:

So, the RBA’s cash rate is now down from 4.35 per cent to 3.85 per cent and the jury is still out on further cuts. So much is happening around the world, and I reckon the RBA is cognisant of how quickly things can change.

Some economists are predicting another four 0.25 per cent rate cuts before the end of the year, while others are forecasting just two more cuts.

So, what to do with those home loan savings from this, and potentially, future rate cuts? Here’s what others are doing and my thoughts, too.

Savings boost

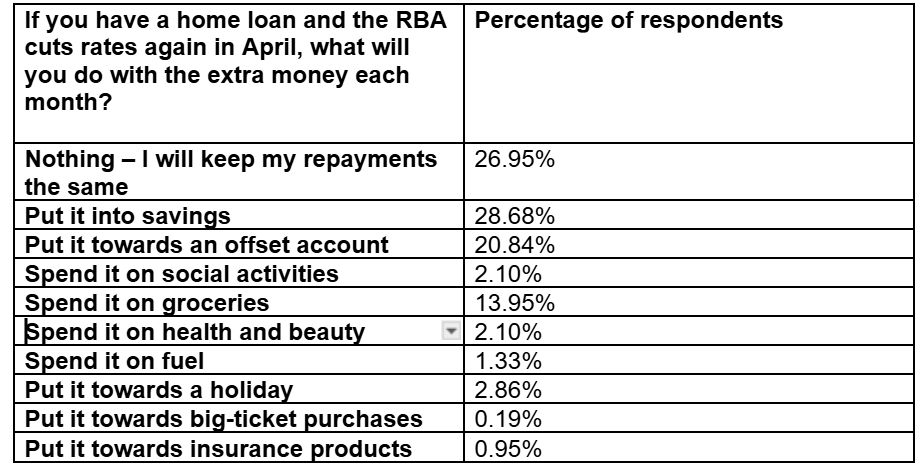

Aussie homeowners will likely “stash” rather than “splash” their savings from the latest RBA rate cut. New Compare the Market research shows most will either boost their savings or offset accounts, or they’ll keep their repayments unchanged.

To put that 0.25 per cent cut in perspective, a borrower with a loan of $666,000 will pocket around $100 a month. That’s more than $1,200 a year.

So if you’ve weathered the previous rate hikes and your budget is still in pretty good shape, it’s not a bad idea to keep your repayments the same, even when your lender passes on rate cuts. About 27 per cent of homeowners told CTM’s survey they would use this strategy to pay down their loan faster.

When you pay off more principal, the size of your loan – and ultimately the interest you pay, will reduce over your loan’s life. My tip is to check if you need to set a new repayment amount with your bank or lender now the savings are passed on, as it may automatically adjust in line with the rate change.

Shop around

Some banks are also offering cashback offers of up to $4,000 if you refinance – another way to grow your savings.

If refinancing is something you’ve been considering, now could be a great time – especially if your current lender tells you they can’t match some of the competitive deals available right now. Time and time again, I see some of the best offers reserved for new customers, so ensure your loyalty isn’t costing you.

There are some fantastic cashback offers popping up. You can essentially lock in a better interest rate and pocket some extra cash. It’s like having your cake and eating it too. Just double-check any applicable fees you may incur to switch lenders, as you don’t want them to gobble your savings up.

Offset or a holiday?

Meanwhile, around one in five homeowners surveyed (21 per cent) say they will put the extra money into an offset account.

When used correctly, offset accounts are a great way to help you pay less interest on your home loan. Whatever amount of money is in your offset account is subtracted from your home loan balance each month. The more money you have in an offset account, the less you’ll pay in interest on your home loan. But remember there are fees associated with offset accounts, so ensure the savings outweigh these costs.

The survey also found around a fifth of mortgage holders would spend the extra money from a rate cut on things like groceries (14 per cent), holidays (3 per cent), health and beauty (2 per cent) and social activities (2 per cent).