The power of interest rises on average Australian families is so much more devastating than it is in other countries.

When our rates go up there is an immediate flow through to household budgets because the vast majority of home loans are variable.

When official rates go up it immediately flows through to loans and repayments.

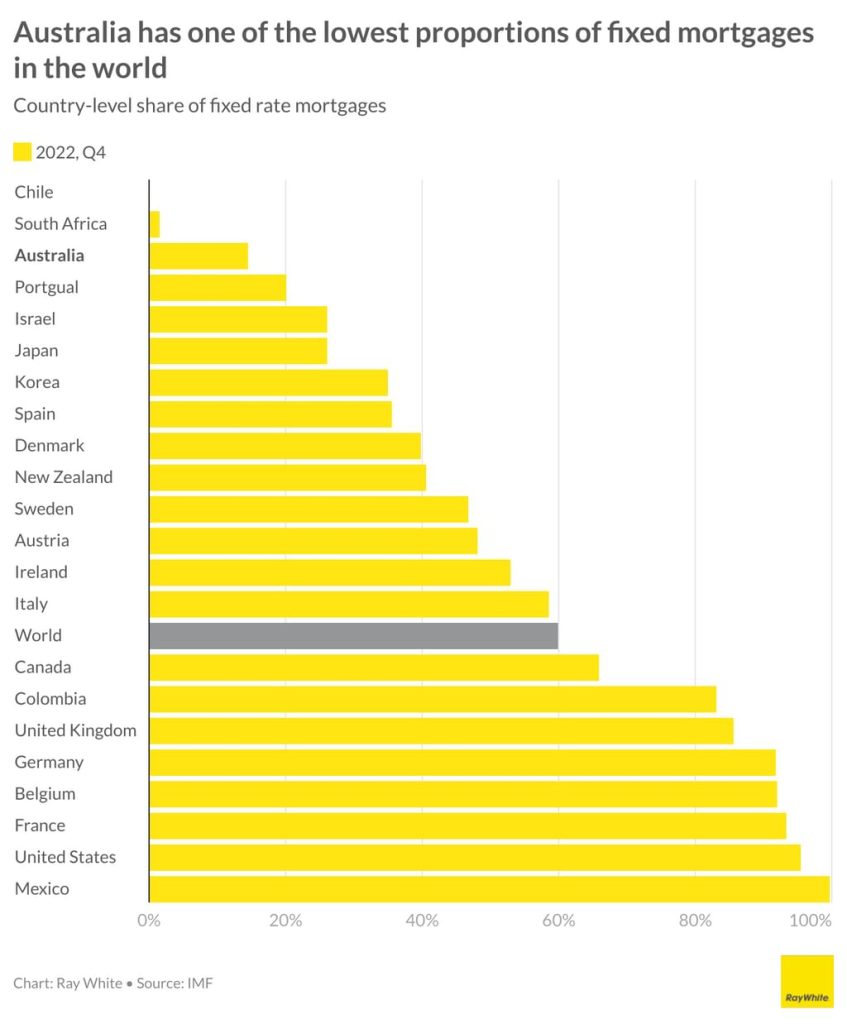

Look at this chart from Ray White chief economist, Nerida Conisbee, where only 15 per cent of home loans are on a fixed rate. Compare that to the global average of 60 per cent and near 100 per cent in the US and Mexico.

In those countries, borrowers don’t feel any rate rise (or fall) until they change properties. In Australia, it’s immediate. That’s why rates are a very powerful tool in boosting or reducing household budgets.

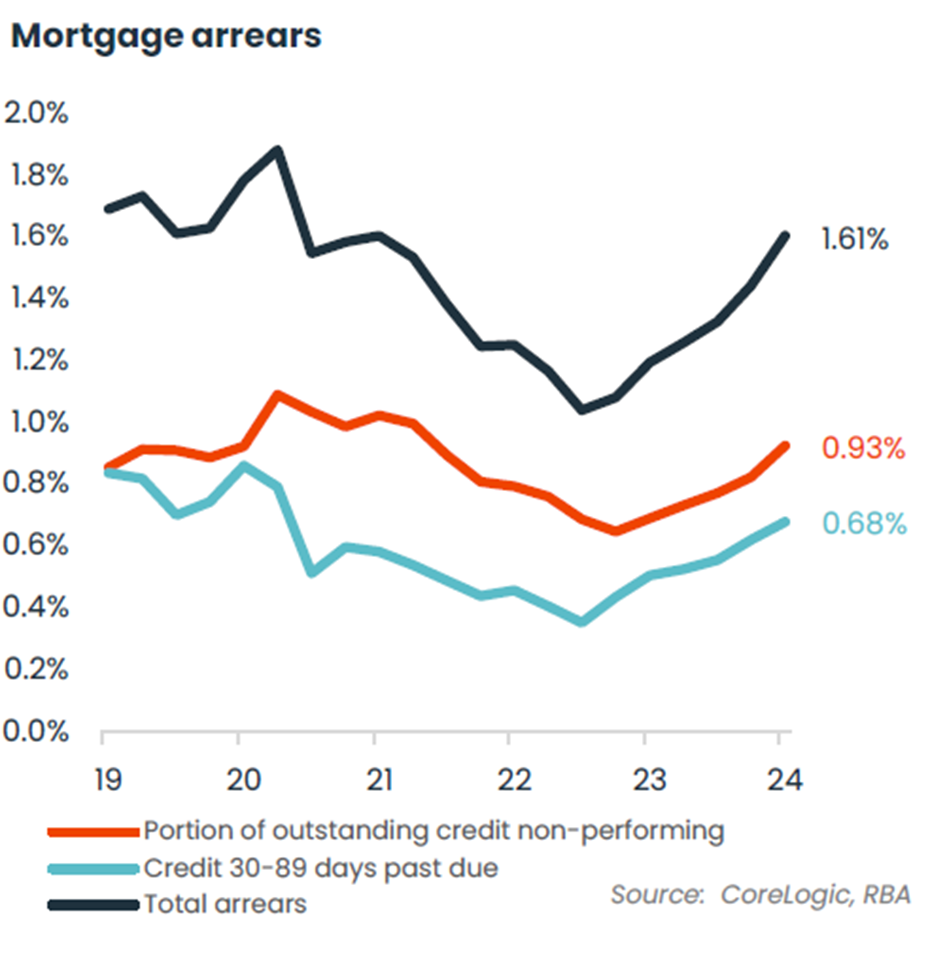

It’s also the reason behind the CoreLogic research which shows mortgage arrears have been rising from their COVID lows of just 1 per cent in September 2022 to 1.6 per cent in this latest March quarter. That is still low but a 60 per cent rise in 18 months.

The upwards trend in arrears has been most influenced by non-performing loans, where the arrears rate has risen to 0.93 per cent. A non-performing loan is one that is at least 90 days past due or where the lender expects it won’t be able to collect the full amount due. The non-performing arrears rate is now slightly higher than it was at the onset of COVID (0.92 per cent) and above the historic average of 0.86 per cent.

A key factor in higher mortgage arrears is, of course, the sharp rise in the cost of debt. With the average variable interest rate on outstanding owner occupier home loans rising from 2.86 per cent in April 2022 to 6.39 per cent in March 2024, a borrower with $750k of debt would be paying nearly $1,600 more each month on their scheduled repayments.

But there are other factors at play as well. Cost of living pressures are consuming a larger portion of household income, households are paying more tax than ever before and household savings are being drawn down, eroding the savings buffer built up through the pandemic.

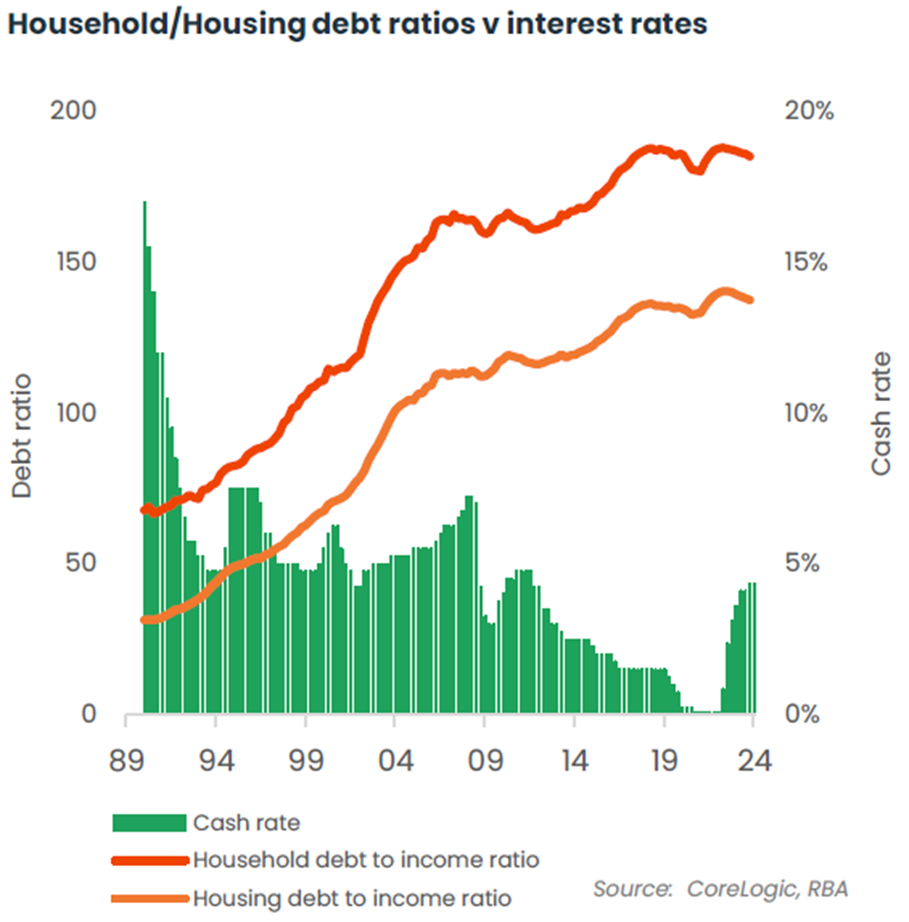

There is also the fact that households are more sensitive to sharp adjustments in interest rates, given historically high levels of debt, most of which is housing debt. Rising unemployment is also spooking Australians.

Australian households are asset rich and cash poor. Their property’s going up in value but they are finding it tough to meet loan repayments. Thankfully, for homeowners that do fall behind on their repayments, there is a good chance most will be able to sell their asset and clear their debt.

The latest estimates on negative equity from the RBA estimate only around 1 per cent of residential dwellings across Australia would have a debt level that is higher than the value of the home. With housing values continuing to rise, the risk of negative equity is reducing.