We all know someone who claims property never goes down and that shares are just a form of gambling. So which is a better investment? Equities or housing?

The right answer, of course, is that both equally play a vital role in building wealth, but they’re very different to each other.

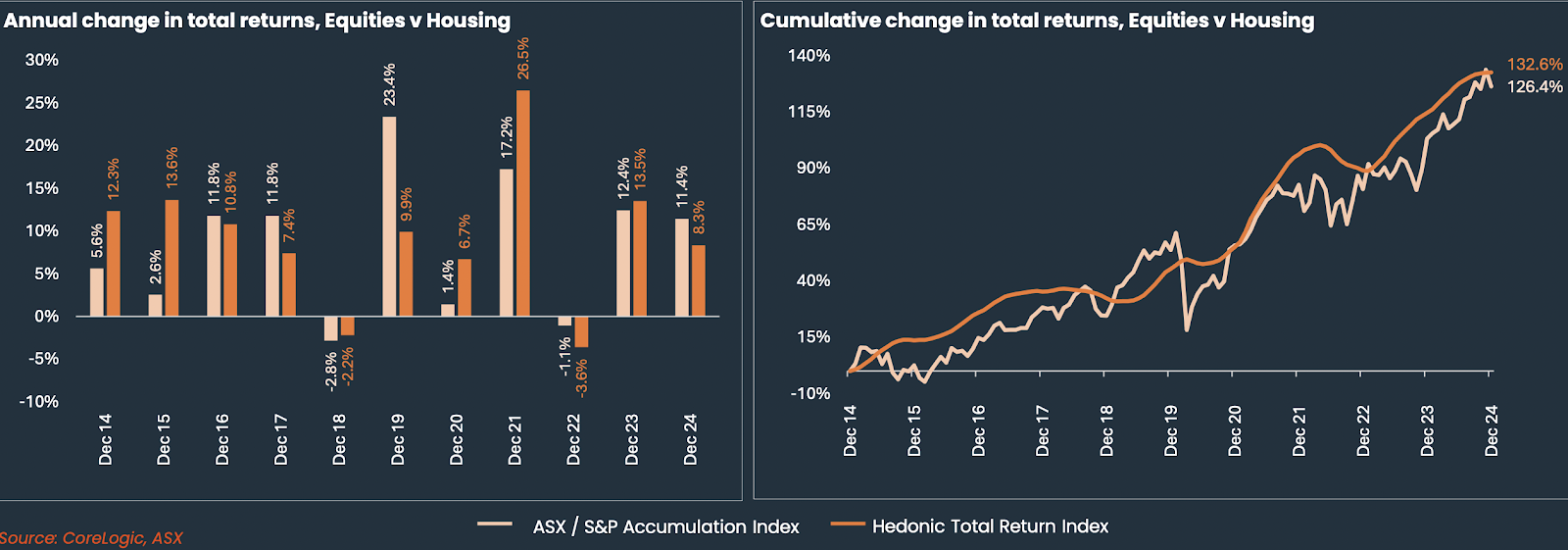

According to property research group, CoreLogic, both shares and residential property had a good 2024 by producing strong returns to investors.

When accounting for capital gains and dividend income, the Australian equity market outstripped property in 2024, with equities up 11.4 per cent over the year, compared to 8.3 per cent growth for property.

But residential real estate continues to underpin Australia’s wealth, estimated at a total value of $11.1 trillion – significantly higher than the combined value of Australian superannuation funds ($4.1 trillion) and the Australian stock exchange ($3.3 trillion).

But of course, investing is a long-term game.

The money marathon

Housing has outperformed equities in six of the past ten years and, cumulatively, has delivered total returns of 132.6 per cent, compared to 126.4 per cent over the past decade.

So, as you can see, both asset classes have delivered great long-term returns.

However, they are both very different asset classes with their unique pros and cons which investors need to weigh up and decide the balance which fits their own individual risk profile and investment objectives.

Anyone who vehemently argues for either shares or property over the other is, in my view, missing the point that they can sit comfortably together in any portfolio.

And, naturally, they both move along their own investment cycle. Some years, like 2024, their investment cycle moves in tandem while in other years they can do the opposite. So it’s important to understand where we are in investment cycles.

Residential property is currently off its peak and trending down. The sharemarket is at record levels but looking a bit shaky.

Here’s a breakdown of the pros, cons, and general performance comparisons to help you decide which option might be better suited to your goals.

Shares (stocks)

Pros:

- Liquidity: Shares are highly liquid – you can buy and sell them quickly on the stock market.

- Low entry cost: You can start with small amounts, unlike property investments which require a substantial upfront capital outlay.

- Diversification: You can invest in various industries and geographies, spreading your risk.

- Potential for high returns: Historically, shares in Australia have averaged returns of about 9-10 per cent per annum (including dividends and capital gains) over the long term.

- Flexibility: No ongoing maintenance or management is required, unlike managing a property.

- Tax advantages: Franking credits on Australian shares can reduce your tax liability.

Cons:

- Volatility: Shares can be highly volatile, with prices influenced by market sentiment, global events, and company performance.

- Complexity: Investing in shares requires research and knowledge to choose the right investments.

- Emotional factors: Price fluctuations can lead to emotional decisions.Residential property

Residential property

Pros:

- Tangible asset: Property is a physical asset that many people feel more secure owning.

- Leverage: You can borrow a large portion of the purchase price, amplifying potential returns.

- Rental income: Provides a regular, steady cash flow if rented out.

- Capital growth: Australian property, particularly in major cities, has experienced significant long-term growth (around 6–7 per cent per annum in some markets).

- Tax benefits: Negative gearing and depreciation can offset taxable income.

Cons:

- High entry costs: Requires a large initial investment, including deposits, stamp duty, and legal fees.

- Illiquidity: It can take months to sell a property, making it less flexible.

- Ongoing costs: Includes maintenance, insurance, property management fees, and council rates.

- Market risk: Property markets can be subject to downturns due to interest rate rises, oversupply, or economic conditions.

- Concentration risk: Unlike shares, it’s harder to diversify when investing in property.

Key influencing factors:

- Interest rates: Rising rates can negatively affect property prices but may not directly impact shares unless they influence broader economic conditions.

- Economic growth: Shares are tied to company earnings and economic growth, while property depends more on demand, supply, and borrowing capacity.

- Leverage impact: While property is more leveraged, amplifying gains or losses, shares can also be purchased with borrowed funds (e.g., margin loans), though this carries higher risk.

Key considerations:

- Risk tolerance: Shares suit investors comfortable with volatility. Property appeals to those seeking stability.

- Time horizon: Shares perform better over a long horizon (10+ years). Property might suit medium-to long-term goals.

- Capital available: Shares require less capital to start, while property demands significant upfront costs.

- Diversification: Shares allow easier diversification as property ties up a large portion of capital in one asset.