Yes, it’s that time of the month when the Reserve Bank decides your mortgage repayments. This time they’ve given us a breather.

On Tuesday, the RBA kept official interest rates on hold at 4.1 per cent. BUT (yes, I deliberately put this in capitals) don’t think this is the end of the rate hike cycle.

Yes, the RBA (I think) did the right thing in pausing after a better-than-expected monthly inflation figure and signs the jobs market is easing.

But those economic trends need to continue for this pause to last longer than a month.

In the RBA statement attached to the decision, the Board noted three key reasons why they kept the cash rate unchanged.

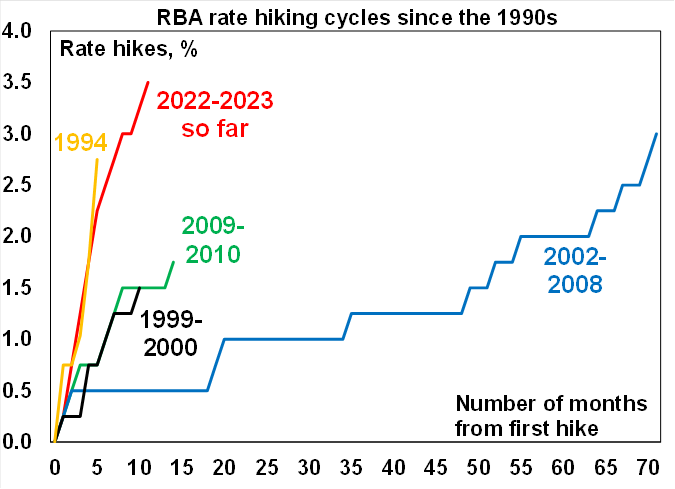

1. “Interest rates have been increased by 4 percentage points since May last year.”

In other words, we’ve seen the biggest and quickest interest rate rise for a generation and it is having an impact on Australians meeting their loan repayments. Business insolvencies are skyrocketing and the economy is still growing, but slowing massively. The RBA doesn’t want the economy to fall off a cliff so is pausing to see more economic data on the slowdown.

2. “The monthly CPI indicator for May showed a further decline.”

As I noted a couple of weeks ago, the monthly CPI decelerated to 5.6 per cent a year in June – down from 6.8 per cent in May and way down on what analysts had forecast. But I mentioned at the time that monthly CPIs can be pretty volatile and that the RBA looks more closely at the quarterly figures. I reckon there’s also concern about the huge number of price rises which came through on 1 July. So, they’ll be watching the upcoming inflation figure like a hawk for any spike up. That downward inflation trend must continue.

3. “The decision to hold interest rates steady this month provides the Board with more time to assess the state of the economy and the economic outlook and associated risks.”

The big one here is the June quarter CPI which is released ahead of the August Board meeting, which will provide the RBA a full assessment of the inflation picture. I reckon that one economic figure will singularly determine the interest rate decision next month.

Importantly the forward guidance from the RBA was unchanged from what was used in both May and June. The same sentence – “some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will depend upon how the economy and inflation evolve” – was retained in July.

The key economic events between now and the next RBA meeting on 1 August will be June labour force data (due 20/7), Q2 23 CPI (26/7) and June retail trade (28/7).

Source: AMP

I know lots of borrowers are breathing a sigh of relief after the rate pause, but that doesn’t mean you shouldn’t keep trying to get a better loan deal.

I love these succinct tips from RateCity on negotiating with your bank. Start at the top and work your way down. Hopefully you’ll have a smaller home loan interest rate when you put the phone down.

3 things you should do before you pick up the phone to haggle:

-

Check what rate you’re currently paying.

-

Check what your bank is offering new customers.

-

See what other lenders are offering and arm yourself with at least two or three rates that would apply to your mortgage.

Now you’re ready to call your bank and haggle.

3 things you can say to get a decent cut:

-

Mention that you’re considering refinancing and list a few lenders and their rates. If you name-drop a couple of competitors, they might be more inclined to take notice.

-

Ask to speak to the retention team – they’re the ones with the license to hand out bigger discounts.

-

If they still don’t budge, ask for a mortgage discharge form. That should be enough to call their bluff.

Get Kochie’s weekly newsletter delivered straight to your inbox! Follow Your Money & Your Life on Facebook, Twitter and Instagram.

Read this next: