The Big 4 bank economists are forecasting interest hikes to begin between June and September. So what should you do to prepare for upcoming increases to your mortgage repayments?

This week’s Reserve Bank (RBA) board meeting, kept official interest rates on hold as expected. But it was their language that attracted attention. Up until now the RBA has been very calm and sanguine about future rate rises, whereas now they are basically saying rate rises are coming very soon.

The Board has dropped its previous monetary policy statements comment that it is “prepared to be patient”.

“Over coming months, important additional evidence will be available to the Board on both inflation and the evolution of labour costs” says RBA Governor, Phillip Lowe, which supports the case for an interest rate hike. He notes that inflation “has picked up” and “a further increase is expected,” but the Board still needs to see wages lift.

And wage rises are coming. There is so much competition for staff as our unemployment rate declined to a 13½-year low of 4 per cent in February. Job vacancies hit a record high of 423,500 available positions in the same month.

While anyone on a fixed rate has bought themselves temporary immunity to any rate increases, variable rate mortgage holders are about to get hit. So start with the interest you’re paying on your existing home loan. If it’s more than 2.09 per cent(which is the lowest Big 4 bank variable rate on offer – see table below), ring up your financier and ask for a discount.

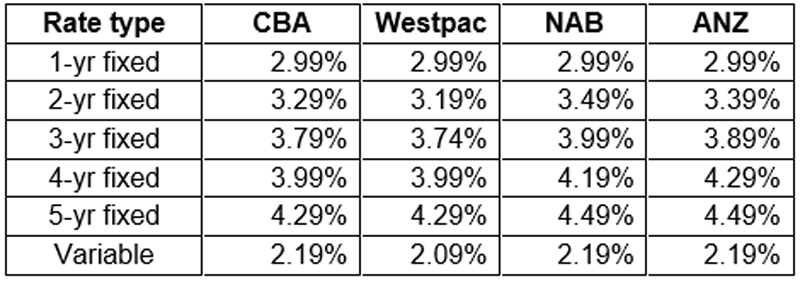

Lowest Big 4 bank owner-occupier home loan rates

Source: RateCity.com.au. Note: Some loan-to-value ratio requirements apply.

Current variable rate analysis

New RBA data out shows the average existing owner-occupier variable rate mortgage customer is on an interest rate of 2.92 per cent. But according to comparison website RateCity.com.au, analysis on variable home loans shows:

- 64 variable rate loans are available from 33 lenders at under 2 per cent.

- 1.79 per cent is the lowest variable rate for owner-occupiers, it’s available from three lenders.

- 2.17 per cent is the average Big 4 bank lowest variable rate, which is 0.53 per cent lower than it was a year ago.

- 38 lenders have cut at least one variable rate for new customers in the last two months, including all Big 4 banks.

The question is: have you received your rate cut? If you haven’t ring them up and ask.

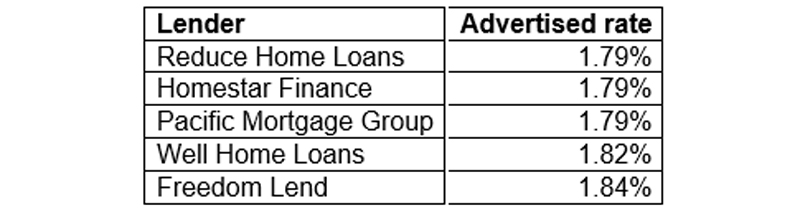

Lowest variable rates on RateCity

Source: RateCity.com.au. Note: Some loan-to-value ratio requirements apply.

Current fixed rate analysis

When it comes to fixed rate loans RateCity.com.au found:

- Six fixed rate loans are available from four lenders at under 2 per cent.

- 144 fixed rate loans are available from 35 lenders under 2.5 per cent (mostly 1-year fixed).

- 3.34 per cent is the average Big 4 bank 2-year fixed rate for owner-occupiers (principle and interest), which is 1.42 per cent higher than a year ago.

- 91 lenders have hiked at least one fixed rate in the last 2 months.

Lowest fixed rates for owner-occupiers

Source: RateCity.com.au. Note: Some loan-to-value ratio requirements apply.

Four things to do to prepare for higher mortgage repayments

Other things to think about when preparing for the upcoming rise in mortgage repayments:

- Do your sums and maybe look at a cocktail of fixed and variable home loans to suit your budget.

- Put in an extra 2 per cent rise in rates (don’t worry, it won’t happen all at once) into your bank’s online mortgage calculator and put that amount away in savings (or extra repayments now to get ahead of schedule) and live on the remainder. That way you’re adjusting your lifestyle now in preparation, so it won’t come as such a big shock.

- Revisit the household budget and see what costs could be trimmed to free up extra cash.

- In this period of labour shortage look at a side hustle to earn extra cash.