The ‘rent or buy?’ question has been a hot one for a number of years now. The deterioration of home affordability because of rising property prices is an ongoing critical issue, particularly among young Australians wanting to buy a first home.

If you’re struggling to meet the market and buy your first home, maybe the solution is… don’t.

Can the solution to the rent or buy stress be that simple? Now that you’re over the shock, think about it. Renting does stack up, but this strategy needs discipline to work.

Discipline is rewarding

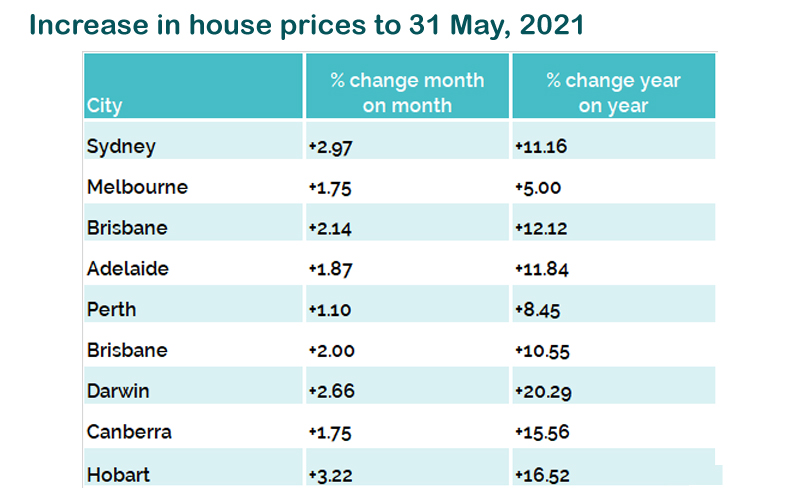

We know Australians love their bricks and mortar, but maybe we take that love affair a little too far. The latest property data suggests that buying their dream home is becoming increasingly out of reach for the average young Australian.

Source: CoreLogic Home Property Value Index [All Dwellings]

But, and this is a big but, renting where it’s cheaper than owning is only a better financial decision if you invest the difference between the cost of renting and the cost to buy.

Invest, not spend

If you blow the money saved from renting instead of investing it, you’re better off servicing a mortgage and having an asset to show at the end of the day. Think of it as enforced saving.

If you do have that financial self control, then renting is probably a better option. We don’t just say that because of the greater financial burden of a mortgage compared to a lease in the current market, but also because of the less tangible benefits.

WATCH: It’s not just the mortgage that makes buying a home expensive:

The opportunity cost of a mortgage is significant. By that we mean that having your money tied up in a mortgage means you don’t have it to spend on other opportunities… Investing in a business, buying shares, funding further education.

While it’s theoretically true that the home you live in is a financial asset, this doesn’t really work if you intend to live in it forever. See, unless you sell it, it’s not really an asset that gives you any true financial benefit.

Greater flexibility

Renting also provides greater flexibility to move for work, upsize your digs for a growing family and move around to find a neighborhood that fits your lifestyle better.

There is also diversification to consider. Often people are so stretched in affording a deposit on a house that they end up with all their savings in one spot; their property. This is a risky investment strategy, because if property prices fall in your suburb, so does your wealth.

Smart investors reduce this risk by spreading their investments across different assets. Investing across shares, bonds and property means that if one market falls, there’s a greater chance those falls will be compensated by gains in their other investments.

However, as we mentioned, this approach only works if you have the discipline to invest the money you save from renting into other areas. The big benefit of buying has always been the way it forces you to save and, if you stick with it, wind up owning an asset.

So really, the answer to the rent or buy question all boils down to self discipline.