How much interest rates will rise is the big question and each of the big banks have a slightly different answer… but they all agree the first rate increase will be June.

Westpac’s economic team is now predicting the cash rate hikes will start in June and hit 2 per cent by June the following year. The bank’s previous forecast had the rate hikes starting in August and reaching 1.75 per cent in February 2024.

NAB has also updated its forecast, with the first cash rate hike starting in June (previously August), while ANZ’s economic team updated its cash rate forecast, bringing forward the predicted start date by three months to June as well.

All four big bank economic forecasts have the cash rate hikes finishing at different points. CBA believes the cash rate will peak at 1.25 per cent, whereas ANZ says the cash rate will rise above 3 per cent… but not until after 2023.

Summary of Big 4 bank’s forecasts:

- CBA: hikes to start in June. Cash rate to reach 1.25 per cent by February 2023.

- Westpac: hikes to start in June. Cash rate to reach 2 per cent by June 2023.

- NAB: hikes to start in June. Cash rate to reach 2.25 per cent by August 2024.

- ANZ: hikes to start in June. Cash rate to reach 2 per cent by November 2023 and peak above 3.00 per cent, but not until sometime after 2023.

If the cash rate reaches 2 per cent by June 2023, as predicted by Westpac, the average owner-occupier with a $500,000 debt and 25 years remaining, could see their repayments rise by $509. This would equate to a 22 per cent rise in monthly repayments from today to mid next year.

Westpac forecasted RBA hikes: impact on $500K home loan

Source: RateCity.com.au. Notes: forecasts are from Westpac’s economic team. Calculations are based on an owner-occupier paying principal and interest with an outstanding debt of $500K over 25 years on the RBA’s average existing customer variable rate of 2.92%.

While there’s plenty of conjecture about how high the cash rate will go, if Westpac is right, it could equate to a 22 per cent hike in mortgage repayments in just over a year. That’s a steep rise, particularly for people with large loans compared to their income.

Interest rates will rise, so build up a buffer

“Now is the time to start battening down the hatches and building up a buffer,” says RateCity.com.au research director, Sally Tindall.

That means mortgage holders should:

- Get yourself a rate cut now before the RBA hikes start: Call your bank and haggle. The average variable rate mortgage holder is paying 0.4 per cent more than a new customer. If your bank doesn’t budge, you could be better off refinancing.

- Make extra repayments: Paying down as much of your debt now, while your rate is still low, will help soften the blow when rates rise.

- Prepare your budget: See where you can trim your budget to free up money to help build a buffer.

- Set a reminder for two months before your fixed rate ends: that way you can begin shopping around for a new loan. Fixed loans often roll over to higher variable rates unless you do something about it.

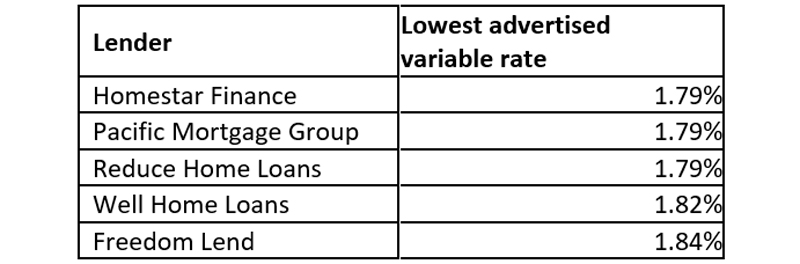

Lowest variable rates on RateCity.com.au

Source: RateCity.com.au. Note: rates are for owner-occupiers paying principal and interest. Some LVR requirements apply.