I’d like to urge you – in the nicest possible way – to consider what will happen to your estate when you die. Yep, dead. Carked it. Fallen off the twig.

I’m not being morbid or funny, but it is going to happen some time and often you don’t have any say in what happens to your money and family after you go. If you don’t think about it now, you could cause your loved ones a mountain of unintended financial pain if the worst did happen.

All this when, hopefully, they are grieving about losing you. In fact, to be honest, you’re a bit of a selfish bastard if you haven’t planned for the aftermath of an untimely demise.

If you don’t have a will

For example, if you don’t have a will the Government will decide who gets your money and when. And it may not be in accordance with your wishes. The thought of your hard earned cash going to a relative you despise should be all the motivation you need to get your affairs in order.

If there are loved ones who depend on you financially, it’s important to structure your affairs to support them if something happens.

So here’s what to do now to control what happens to your estate when you die. Then you can get on with living.

1. Review your affairs

The first step is to review your financial situation to make sure everything is in order.

That means getting an understanding of what assets you own, whether you own them outright or jointly, and whether they will form part of your estate when you die.

If you have a partner, make sure to include them during this process. They need to know how to access your accounts, where the important documents are kept and how to contact anyone who manages your money (such as a financial adviser, accountant or super fund).

Make sure that copies of all your important documentation are stored safely and are readily available.

2. Get super and life insurance sorted

Don’t forget about your superannuation and life insurance during this process. It’s possible to make a binding nomination on who you want these assets to go to in the event of your death, which will override whatever’s set out in your will.

It’s also worth reviewing the level of life insurance cover you have and double-checking that it’s still right for your situation.

Ideally, a life insurance payout will be able to cover any liabilities (debts) you have, as well as provide a lump sum to cover any ongoing costs for family who depend on you.

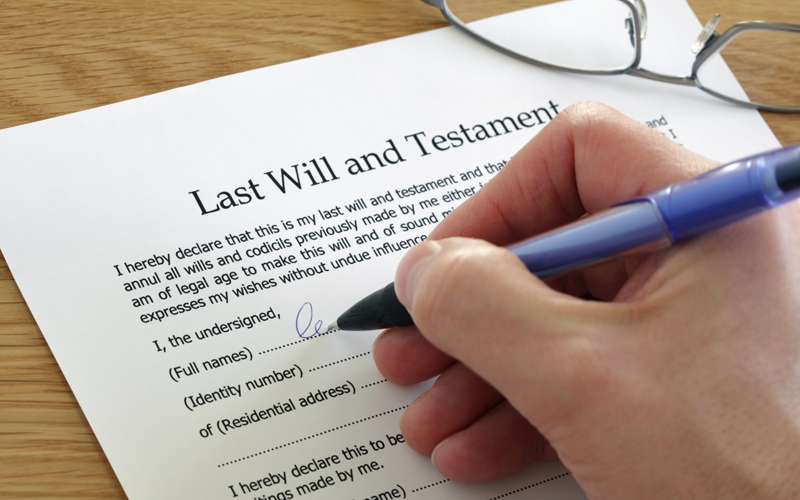

3. Organise your will

A will is a legal document that details how you want to distribute your estate when you die. It can be used to assign guardianship of your children, set up a trust, and provide instructions on your funeral arrangements.

It absolutely staggers me that up to 52 per cent of Australians don’t have a will. Mostly because they ‘haven’t got around to it’. This is just plain stupid.

Wills need to be written, signed by the testator (you) and witnessed by two people who are not beneficiaries of your estate. You also have to name one or more executors to carry your directions out.

The executors do all the hard work, so many experts advise to have two. A friend or relative to deal with the family and a solicitor or accountant to do all the legal statutory work.

While it’s possible to buy ‘do it yourself’ will kits, professional help will ensure that your will is legally binding and your wishes will be carried out as intended.

Always make sure to review your will regularly. This is particularly important after major life events like getting married (which will invalidate your previous will), divorced (which won’t), having a baby or buying a property.

Read this too: How to talk to your parents about their will (without sounding like a gold digger)

4. Powers of Attorney

In some situations, you may want to set up a trusted person with a Power of Attorney to make decisions on your behalf.

A general power of attorney will allow someone to make financial and legal decisions on your behalf when you are unable to manage your affairs through circumstance, such as being overseas.

On the other hand, an enduring power of attorney will allow someone to make financial and legal decisions for you if you become incapacitated. A medical power of attorney will let them also make medical decisions.

5. Get professional help

If your financial affairs are complex it’s worth enlisting professional help. You might have a large estate or own a private business and you might want to minimise the tax implications for your beneficiaries. Or you want to be sure your wishes are carried out as intended.

An accountant or financial planner can provide advice on estate planning. Then engage a solicitor to formalise the documentation.

6. Tell your family

The final thing I would recommend is to sit down and talk to your loved ones about your plans.

We know lots of people keep their will secret as an incentive to keep their adult kids in line. However, that runs the risk of splitting the family and causing huge tax problems. It can even prompt huge court cases which can run for years.

So sit the family down and be open about it.

Trending

Sorry. No data so far.