Almost a quarter of homeowners are worried they’ll have to sell, or have already sold, due to the rising cost of living.

According to a new Compare the Market (where I am Economic Director) survey, most homeowners aren’t worried about having to sell (79 per cent), but a startling 39 per cent of renters fear their landlord will have no other choice… and potentially leave them homeless.

This comes as SQM Research revealed the number of residential properties sold under distressed conditions in Australia has risen to 5,252, reflecting a 2.4 per cent increase.

This is the domino effect following the fixed rate cliff. Many people’s savings buffers have been depleted, and now they’re struggling to meet repayments.

But a forced sale is really the last resort – most homeowners will fight tooth and nail to hold onto their properties.

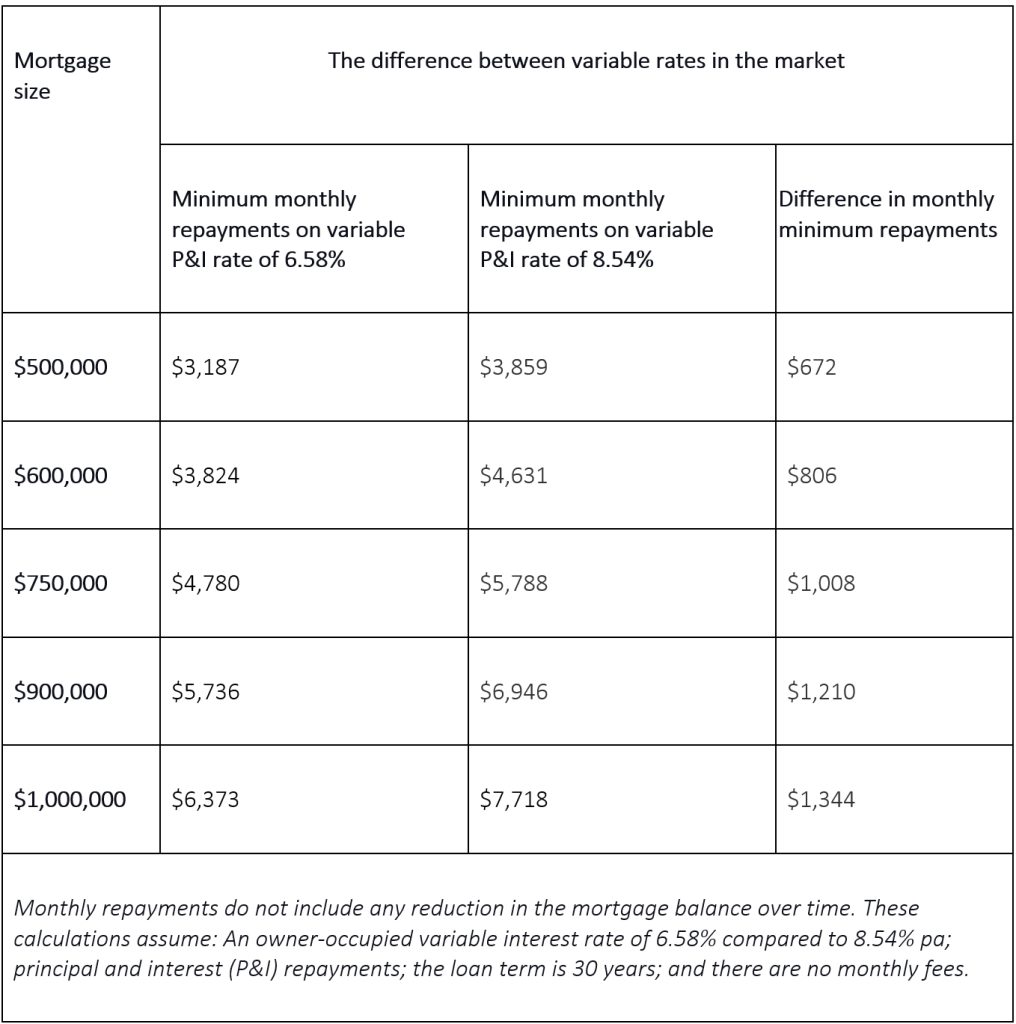

Front-book vs back-book rates

We know tax cuts are coming in July, which should provide some relief. Any cut to interest rates will also help ease the pain of homeowners.

When interest rates fall, property prices are tipped to increase even further, so that’s something homeowners should be aware of as well.

But borrowers need to be proactive and make sure they’re on a low rate now. Some people could be paying hundreds extra per month because they’ve rolled off a low front-book rate (which they received as a new customers) onto a high back-book rate.

If you’ve been with your lender for a while, there’s a strong chance you’re on a high back-book rate.

Compare the Market analysis of some of the rates available from the big four banks showed the average difference between front-book (for new borrowers) and back-book rates (for existing loyal customers) is a whopping 1.96 per cent.

That’s equivalent to eight RBA rate cuts of 0.25 per cent.

Therefore, a person with an owner-occupier $750,000 loan could be saving $1,008 a month when they switch from a rate of 8.54 per cent to 6.58 per cent.

Source: Compare the Market

If you can’t refinance to a lower rate because you no longer meet eligibility criteria, have a crack at negotiating your own rate cut with your current lender.

Find the lowest rate your lender offers and ask them to match it. Homeowners should always be sceptical of their current interest rate and use websites like Compare the Market to make sure it’s competitive.

Five ways to ease mortgage stress

1. Try to negotiate a lower rate

Just one in three Aussie mortgage holders have tried to negotiate a lower rate this year, according to Compare the Market research.

Amazingly, 70 per cent of those that called their lender said they were successful in securing a discount. It shows a simple phone call could end up saving you thousands.

2. Consider asking your lender for financial assistance

But if you’re still struggling to meet mortgage repayments, ask your lender for support. This could include special payment plans, fee relief and rate concessions.

If you’re concerned, don’t try and hide and think your lender won’t notice. They want you to talk to them about what support might be available and to work together on a plan.

3. Switch to interest-only repayments

Switching to interest-only repayments is one way to temporarily lower your repayments. While banks typically don’t like giving owner-occupiers interest-only home loans, they are usually willing to work with you through the tough times.

People on interest-only loans don’t pay anything off their principal, may face higher interest rates, and face a greater risk of negative equity. That said, if you’re struggling to meet your repayments, switching to interest-only may help you keep your house.

4. Request a longer loan term

If you’ve had your home loan for five years or more, you could ask your bank to reamortise your loan over a new longer period.

Lenders need to weigh up a number of risks to decide if you are eligible for this. There is also a fee you usually pay to reamortise your mortgage. The fee varies from lender to lender, ranging from $250 to $500.

While this is one way to gain immediate relief, prolonging your mortgage means you’ll pay thousands of dollars more in interest over the life of your loan. If your financial situation allows, you can switch back to a shorter loan term to save in future.

5. Access free financial debt counselling

The free National Debt Helpline offers advice to people struggling with bills, fines, and repayments. They can help you develop a budget, and explore different options, and advocate on your behalf to other creditors. Contact the helpline on 1800 007 007 (Monday to Friday, 9.30am–4.30pm).

Get Kochie’s weekly newsletter delivered straight to your inbox! Follow Your Money & Your Life on Facebook, Twitter and Instagram.

Read this next:

Here’s what to do if you’re stressed about money – no Squid Game massacre required!