There are benefits for home owners during a property boom. One is that the equity in your property rises, adding to your wealth.

While the value of a loan basically stays the same, or reduces if you’re on a principle and interest loan, a rising property market means the share you own in your place goes up as well.

This increasing equity opens up all sorts of options. They include borrowing against your loan to invest elsewhere, or refinancing your existing loan to a better interest rate because you have more assets.

Loan-to-value ratios are falling

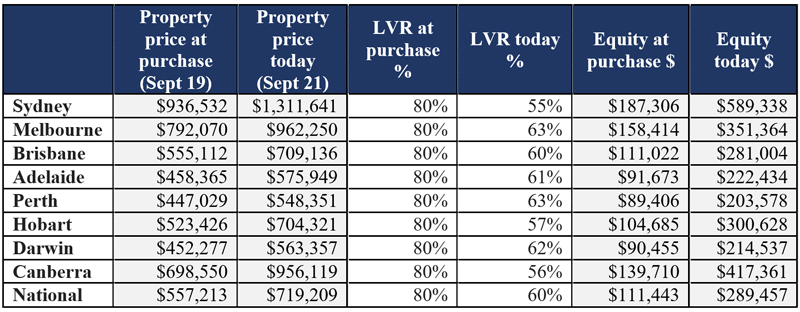

Research from RateCity shows that in Sydney an owner-occupier who bought a median-priced house in September 2019 with a 20 per cent deposit, paying principal and interest on a 30-year loan term, has experienced a $402,032 increase in equity. Their loan-to-value ratio (LVR) has fallen from 80 per cent to 55 per cent.

In Melbourne, an owner-occupier who bought a median priced house in September 2019 with a 20 per cent deposit, under the same terms, has experienced a $192,950 rise in equity. Their LVR has fallen from 80 per cent to 63 per cent.

“Millions of homeowners are sitting on a growing mountain of equity, some without even realising it,” says Sally Tindall, research director at RateCity.com.au.

The RateCity database shows 58 per cent of the lowest variable rates are only available to people with big deposits of 30 per cent or higher, including CBA, Westpac, St George, BOQ, Bendigo Bank and Macquarie.

Owner-occupier purchasing the median-priced house – September 2019

Source: CoreLogic. Starting with 20% deposit

Some of your options to use that increased equity are:

Borrow more

People who have seen their equity rise can potentially borrow additional money from the bank for big ticket items. That might be a home renovation or using your home equity to invest in property or shares.

Note that any loan increase would still be subject to the bank’s serviceability tests. The maximum loan size is typically limited to 80 per cent of your current house price.

Apply for lower rates

58 per cent of the lowest variable rates are available to borrowers with loan to value ratios of 70 per cent and under.

“If you’ve owned your own home for at least a couple of years, and have been diligent about paying down your debt, you could refinance to a lower rate,” says Tindall. “Lots of lenders offer interest rates discounts to new customers with loan to value ratios below 70 per cent, including big four banks CBA and Westpac.”

Remove your guarantor

First home buyers who used a guarantor could reach a loan to value ratio of 80 per cent earlier than expected. You can then apply for the condition to be removed from their mortgage.

Switch lenders

Customers who don’t yet own 20 per cent of their home typically don’t switch lenders because they would have to pay lenders’ mortgage insurance again. The increase in equity helps borrowers who started with a small deposit switch lenders sooner.

A final word of caution

Don’t go too crazy unlocking the equity in your home.

“What goes up can also go down,” cautions Tindall. “If the market takes a dip, the proportion of your home you own will also drop.”